NAV Financing: How Funds Deploy Liquidity

How NAV lending gives small and mid-market private equity funds flexible, fund-level financing to control exit timing, fund follow-on investments, and bridge liquidity gaps without forced asset sales.

Fresh fund launches, add-on capital deployments, and portfolio company working capital demands can all create liquidity requirements that do not align neatly with realisation schedules

This is now a well-established market segment, with more than $850bn in outstanding commitments and approximately 30% of new activity falling outside traditional subscription facilities

The value proposition is most compelling for smaller and specialist fund operators, though agile and efficient processes are essential

Established market participants frequently lack the speed of execution or appetite for smaller transaction sizes

Nodem Capital delivers rapid, tailored financing for small and mid-market borrowers, with committed capital readily available

What was once regarded as a specialised corner of the market—primarily limited to capital call facilities for the largest private equity sponsors—has evolved into a substantial financing ecosystem. The fund finance market now stands at approximately $850bn in aggregate volume, offering a comprehensive range of borrowing solutions to private equity and private credit funds as well as their limited partners (LPs).1

Historically, the bulk of fund-level borrowing was designed to smooth the cash flow mismatch between LP capital contributions and a fund's deployment needs during its earlier years. Such facilities tend to be short-dated, essentially bridging committed capital, and are typically extended by banks to their most significant sponsor relationships.

An increasingly established market

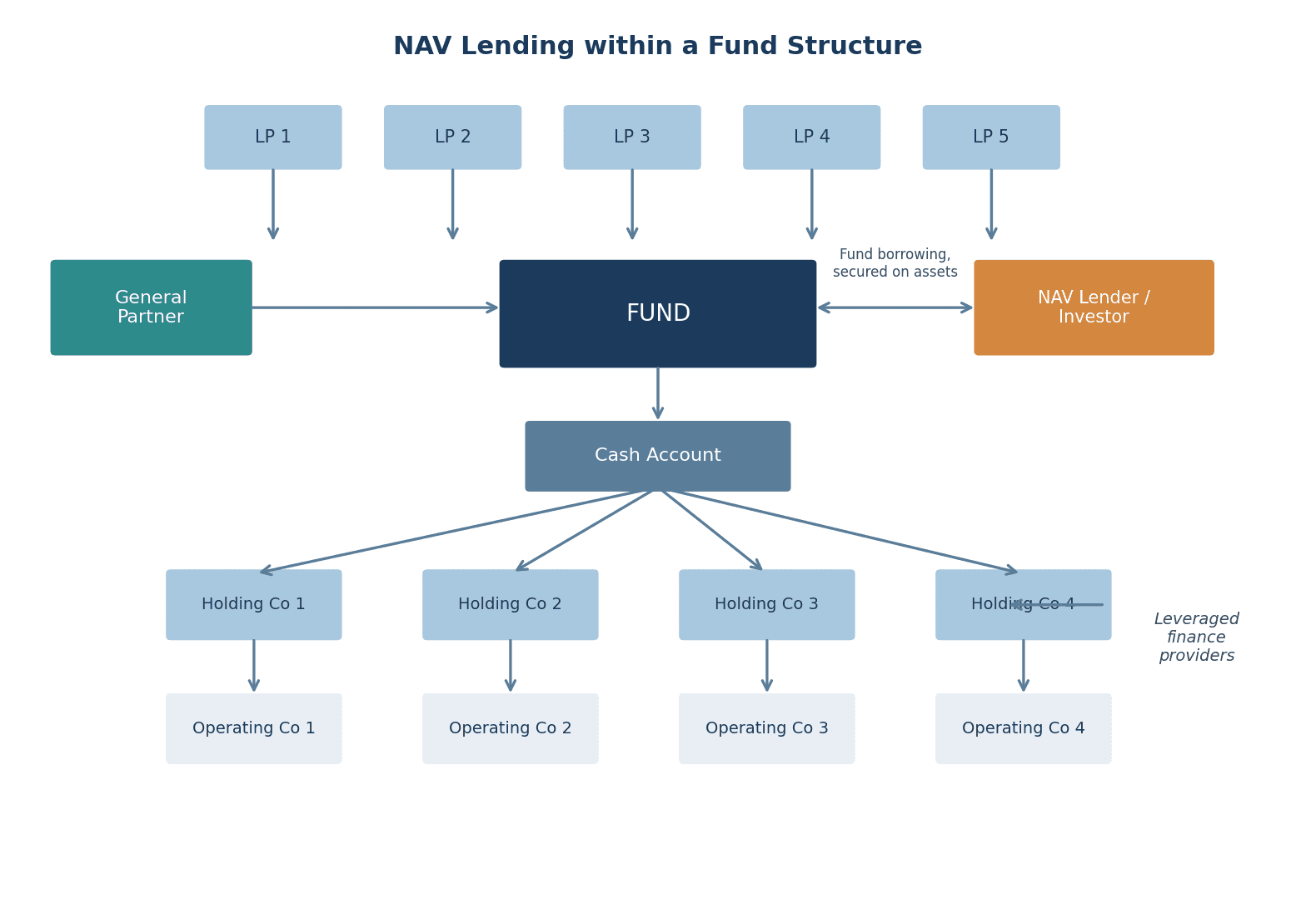

Over the past half-decade, fund financing has matured into a versatile liquidity instrument deployed by both fund managers and investors of all scales, throughout every phase of a fund's existence. The contemporary fund finance landscape provides GPs and LPs with a broad menu of purpose-built borrowing solutions. In contrast to subscription facilities—which are collateralised by unfunded LP commitments—NAV-based lending is secured against the equity value of a fund's underlying portfolio holdings, thereby expanding leverage options beyond the capital call window or in circumstances where drawing on LP commitments would be impractical.

With around 30% of all fund finance activity at the beginning of 2025 falling outside conventional subscription lines, these bespoke arrangements have steadily gained traction as their practical benefits become more widely recognised among fund managers and investors alike.1

NAV-based financing as a bridge across liquidity gaps

The adoption of NAV facilities continues to gather pace. According to Rede Partners, NAV loans now account for roughly $100bn—or about 20%—of the entire fund finance market as of early this year. Separate estimates from Standard & Poor's suggest the figure may have reached as much as $150bn by now. This represents close to a tenfold expansion in market share within just five years, with much of the initial acceleration occurring during the pandemic, when participants sought creative responses to unprecedented conditions.

As both the pace of PE exits and the tempo of new fundraising slowed in recent years, funds and LPs have increasingly relied upon the fund finance market for solutions. The disruption of conventional exit channels—including public listings and trade sales—compelled PE firms to retain portfolio assets well beyond their anticipated holding periods, materially reducing the flow of distributions that investors had come to depend upon. Concurrently, the formation of new funds has become more challenging, as institutional investors defer fresh commitments while awaiting realisations from earlier vintages.

Against this backdrop, NAV lending has emerged as a practical and readily accessible mechanism for funds and their investors to bridge these liquidity shortfalls, avoid premature or value-destroying disposals, and maintain the execution of their asset allocation strategies.

Case study: NAV facility to support add-on investments

A fund manager required $30m to make additional investments across several portfolio holdings. While adequate and well-diversified collateral existed, the quantum of the borrowing fell below the threshold at which most specialist lenders would engage. Nodem was able to complete its assessment and structure a facility secured against a mixed collateral pool comprising fund interests, private company equity, and fine art.

Beyond NAV facilities and conventional subscription lines, a significant share of the fund finance market consists of hybrid structures and LP-level lending. Hybrid facilities blend the characteristics of a capital call line—such as advances against unfunded commitments—with those of a NAV loan, enabling borrowing against the fund's portfolio value. These combined structures can enhance GP flexibility across the full fund lifecycle by offering greater control over portfolio loan-to-value ratios while eliminating the administrative burden of managing multiple lending relationships with differing terms.

LPs, too, have increasingly turned to bespoke hybrid borrowing arrangements to address their own liquidity requirements. LP-level facilities are designed around the specific needs of individual fund investors, with the borrowing secured against the investor's position in one or more PE funds. Critically, the use of proceeds remains unrestricted and need not be connected to the fund against which the facility is collateralised.

Figure 1: NAV lending within a fund structure

New entrants bring greater flexibility

The ongoing evolution of the market—and the proliferation of product types—reflects the broadening profile of the lenders and capital providers now active in the space. In a recent industry survey, bank and non-bank lenders held roughly equivalent market shares, though 80% of newly originated facilities were arranged jointly by banks and alternative lenders at initial closing.2

Unlike traditional bank lenders, which may be constrained by standardised credit frameworks and conventional risk models, the alternative lending community within fund finance is frequently able to offer highly customised solutions engineered for each borrower's particular situation. While such borrower-centric, individually structured financings were harder to access in earlier years, the maturation of the market now enables private equity GPs and LPs of all sizes to treat this form of borrowing as a proactive commercial tool—one that drives transactions and facilitates outcomes, rather than merely smoothing cash flows or serving as a defensive capital buffer.

The financing requirements of mature portfolios that sit outside the capital call window—or at the tail end of a fund's stated life—have historically been underserved, owing to both the modest scale of such borrowings and their mismatch with the minimum facility sizes favoured by conventional lenders. Late-stage and wind-down funds have traditionally found financing options scarce when only a handful of residual holdings remain, given the formulaic collateral criteria of many established providers. Even as fresh capital flows into the fund finance sector, the preference among lenders continues to tilt toward larger borrowers. As average fund sizes have grown markedly compared to earlier vintages, the proportionate borrowing needs of these larger vehicles have increased in tandem.

Our own experience, however, demonstrates that older vintage, mid-market funds holding fundamentally sound businesses can unlock and generate meaningful value through the considered deployment of NAV-secured lending.

NAV loans as a tool for preserving control and timing

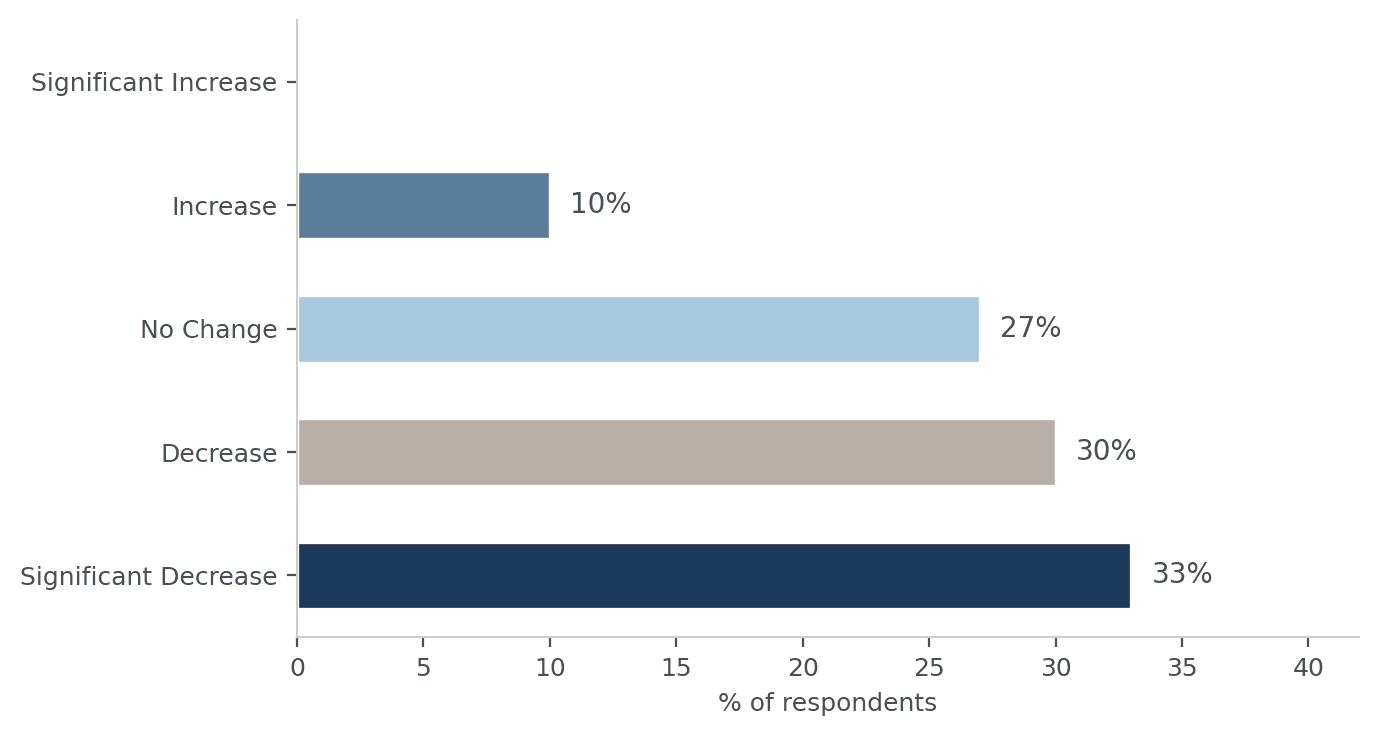

As the adage suggests, the true significance of capital often lies not in its quantum, but in the control it affords. In practice, the principal application of NAV-based lending is as an instrument of portfolio management—preserving autonomy over the cadence of investments and realisations, and safeguarding valuable optionality. The use of NAV facilities specifically to fund LP distributions is considerably rarer than commonly assumed. In many respects, this represents one of the less strategically impactful uses of portfolio leverage relative to other value-enhancing applications, and the proportion of facilities dedicated solely to distribution funding is strikingly modest. Only around a third of outstanding NAV loans were arranged for this purpose, and the broad consensus among market participants is that this share continues to decline.

Survey: Observed trend in the share of NAV loans deployed for distribution purposes. Source: Rede Partners, 2025

More constructively, NAV financing enables funds to operate in accordance with a sound investment principle: that the merit of an opportunity should be assessed on its intrinsic fundamentals, rather than being dictated by the vagaries of capital flows or financing constraints. Access to fund-level borrowing widens the universe of actionable options and empowers a manager or investor to retain control over the timing of disposals and exit events. The flexibility afforded by NAV-based lending can facilitate the pursuit of new opportunities and prevent the forced sale of holdings at an inopportune moment.

Case study: NAV lending to safeguard optionality and control

Nodem Capital recently partnered with a seasoned private equity fund holding three residual portfolio assets with an aggregate value of approximately €500m. Working capital requirements at the portfolio company level, together with the need to refinance maturing debt, created a near-term cash requirement of around €30m.

Sourcing this liquidity might have necessitated a capital call on LPs. Given the advanced stage of the fund, this route was viewed as both operationally inefficient and time-consuming. The alternative was to accelerate the marketing of one or more assets ahead of the manager's planned timeline—with predictably adverse consequences for value maximisation.

Instead, the €30m was raised through a NAV facility, extending the fund's liquidity runway from less than a month to two years. The low loan-to-value ratio meant the facility required minimal covenants, allowing the GP to retain full operational flexibility. Although the interest rate carried a premium relative to a bank facility, the all-in cost of arranging the NAV loan was below 2% of NAV.

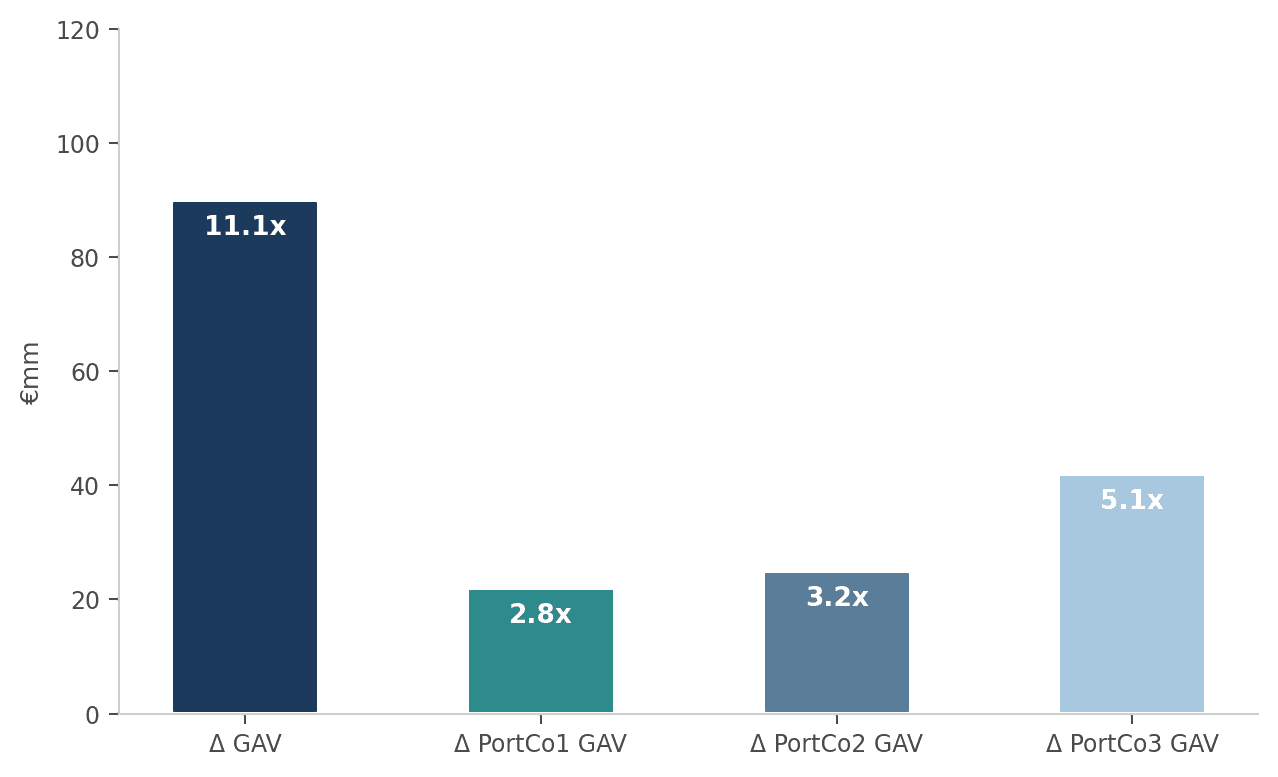

The pricing reflected the fund's pressing timeline (which compressed the due diligence window), the concentrated nature of the remaining portfolio, and the short tenor of the facility. Crucially, however, by employing a creative financing approach, the fund ultimately exited its investments at 2.2x tangible value—materially above the indicative bids of under 2x that had been quoted for an expedited sale. The net impact on portfolio returns amounted to as much as +22%, underscoring the significant value that can be preserved through maintaining optionality and control over exit timing.

NAV facility cost relative to portfolio value uplift

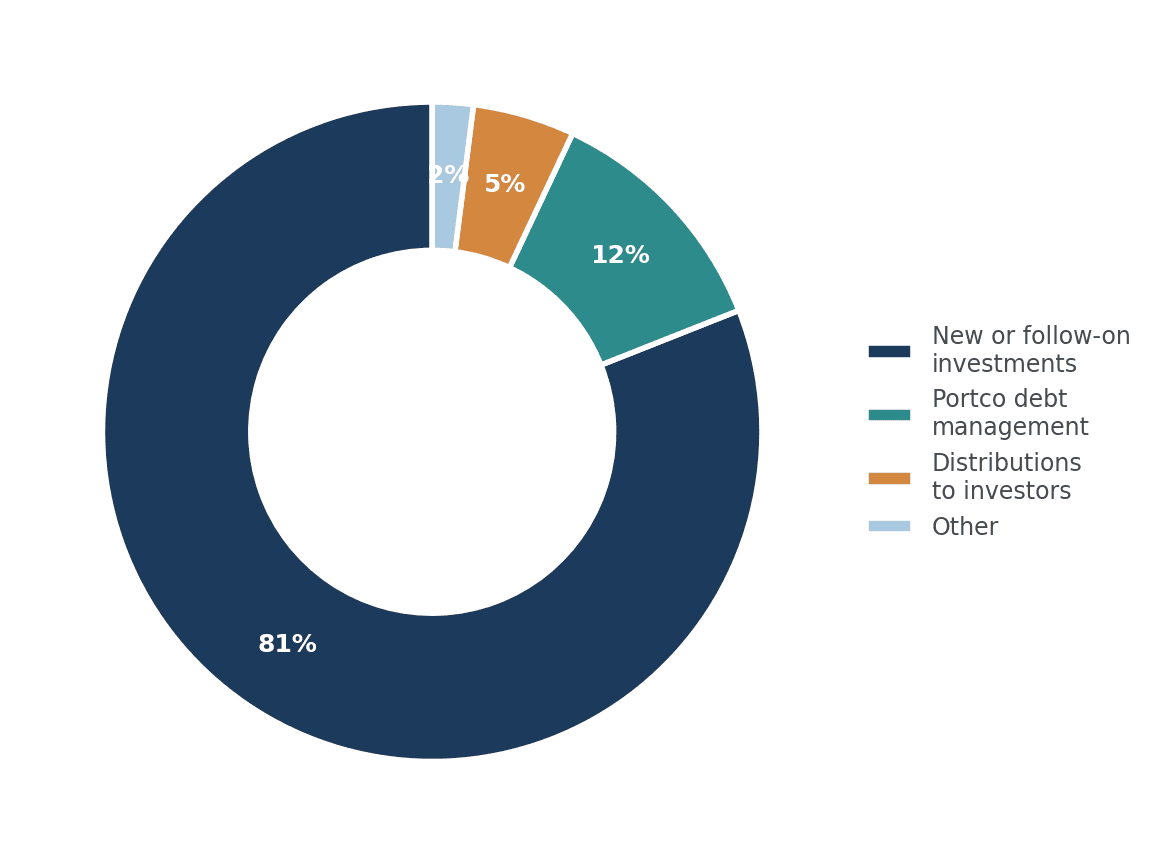

Indeed, the largest share of NAV facilities is directed toward financing new or follow-on investments, with the next most prevalent application being the refinancing of portfolio company obligations or management company leverage. The evidence consistently indicates that NAV lending serves primarily as a tool for expanding the investment opportunity set, rather than as an exercise in financial engineering. The data also suggest that borrowing behaviour remains conservative by most measures—over half the loans in the Fund Finance Partners NAV Loan Index were originated at loan-to-value ratios below 15%, with an average of ten distinct underlying assets in the collateral pool.

Figure 2: Allocation of NAV lending proceeds. Source: NAVember.

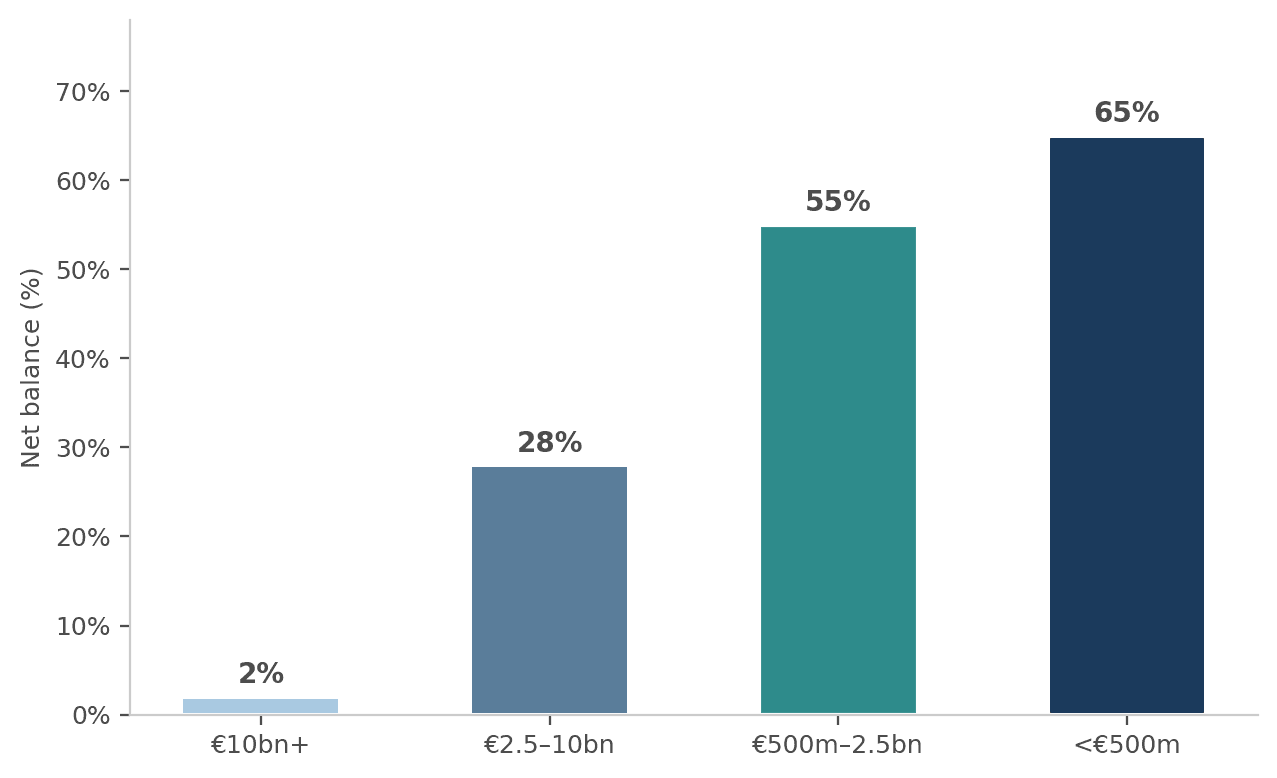

NAV loans: Closing the gap for smaller fund managers

This pattern implies that access to debt financing may hold disproportionate value for smaller funds, where the capacity to capitalise on time-sensitive opportunities can have a more meaningful impact on overall performance. Historically, however, achieving this has proved difficult. The NAV financing market originated with banks, where fixed costs relating to overhead and administration undermined the commercial viability of smaller-ticket facilities.

Even as NAV lending has evolved from a reactive liquidity mechanism into a proactive strategic tool—and has attracted secondary and private credit funds as active participants—the capital providers entering the market have predominantly been larger GPs. Fund launches since 2020 have reflected this scale dynamic, with vehicle sizes typically ranging from $500 million to $2.5 billion.

Case study: Financing a GP commitment

A well-established specialist private equity manager sought to pre-fund the launch of its third vintage, aiming to demonstrate commitment and attract capital from both returning and prospective LPs. The GP held substantial assets in the form of carried interest, excess management fees, and stakes in prior vintages, but these proved challenging for conventional banks to underwrite—while the transaction size was too small to attract the larger specialist lenders. Nodem Capital drew on its expertise and structural flexibility to arrange a tailored borrowing facility, advancing between $15m and $20m for a period of less than two years, providing the GP with adequate runway to complete the fundraise.

A practical consequence of the increasingly large vehicles now active in NAV lending is that fewer capital providers are willing to engage on transactions where the facility size falls below approximately $30–40 million. Loans of this magnitude—particularly when they refinance or roll over after a relatively brief period—have limited impact on the returns of a large fund, yet demand a comparable quantum of legal and analytical work to that of a substantially bigger facility. As a result, the principal participants in private NAV lending have gravitated toward the upper end of the market, where they can deploy meaningful sums annually through a small number of transactions.

While this dynamic is beginning to shift as the market continues to mature, for now only a handful of lenders are operationally structured and committed to delivering the rapid execution, covenant flexibility, and structural adaptability that best serve smaller GPs or those with more modest borrowing requirements.

Rising adoption of NAV facilities is most pronounced among smaller funds. Net balance (share reporting an increase less share reporting a decrease). Source: Rede Partners 2025

Practical applications for NAV facilities below $40 million

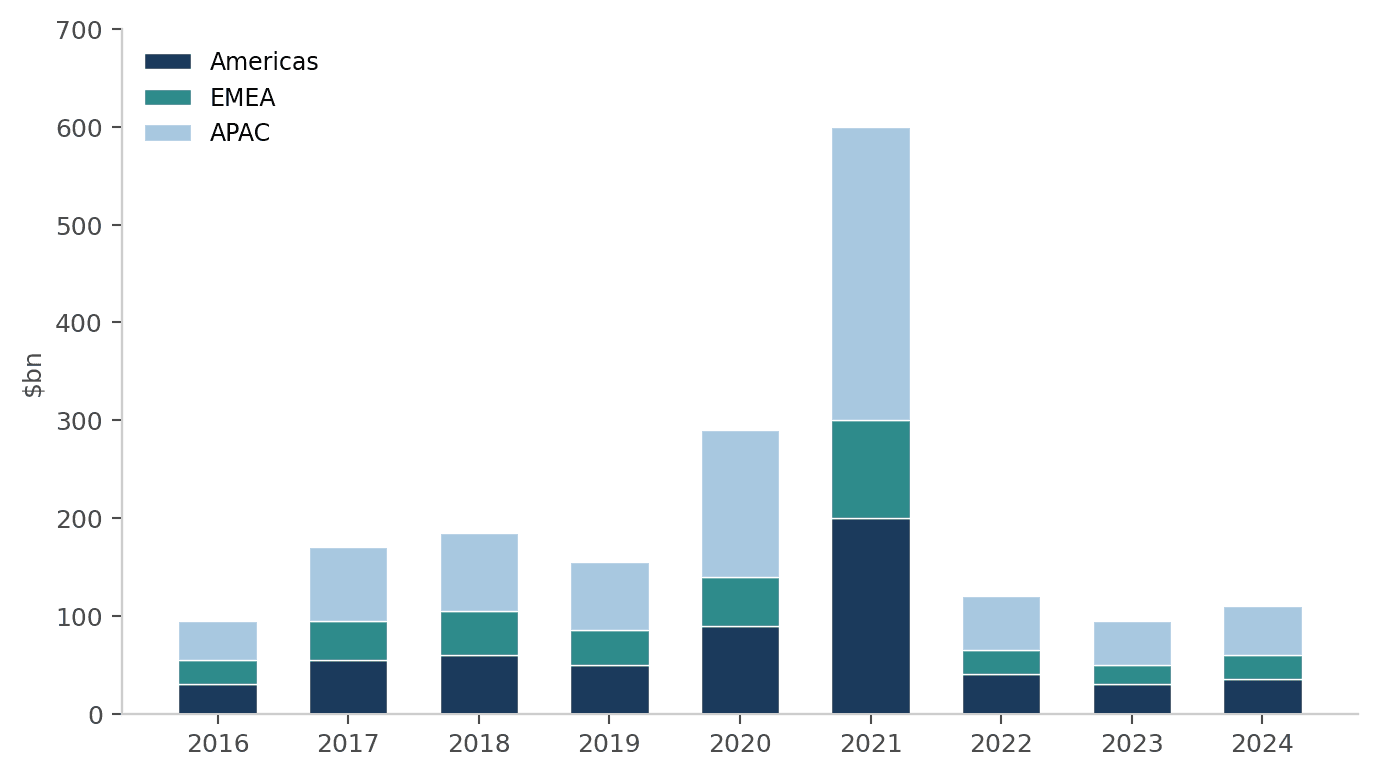

Seeding new fund vintages: Following the successful maturation of a fund, a manager's opportunity set and fundraising reach for the next vintage will typically have expanded, making it logical to grow fund sizes progressively in order to capitalise on deeper experience and broader sourcing networks. Yet the optimal timing for a new fund launch and its initial deployments should, ideally, be governed by the quality of the investment pipeline—not by the realisation schedule of predecessor vehicles. This consideration is especially pertinent in an elevated rate environment, where subdued M&A and IPO activity may extend fund lifespans and require longer holding periods in order to deliver the best outcomes for investors.

Figure 3: Worldwide IPO activity ($bn)

Investors frequently expect to see a meaningful personal commitment from the GP in any new fund, as a signal that incentives are closely aligned. But for the reasons outlined above, launching a larger successor fund while the prior vehicle has not yet fully liquidated can create genuine cash flow challenges. By borrowing against the NAV value of their interest in the earlier vintage to finance their commitment to the next, managers are temporarily increasing their personal portfolio leverage. This mechanism not only bridges the cash flow gap but also transmits a powerful signal of conviction to both prospective and existing investors regarding the manager's confidence in generating returns across both vehicles.

Strategic and opportunistic portfolio company investments: When a fund is fully—or nearly fully—committed, situations may arise in which certain portfolio companies require supplementary funding to reach a successful exit. Arranging new debt or refinancing existing obligations at the portfolio company level is often administratively burdensome, particularly where the original borrowing was structured on a long-term basis but only requires a short-term extension, or where only a marginal amount of incremental capital is needed. In these circumstances, a NAV-based solution—entailing a loan originated at the holding company level and secured against a diversified portfolio—can be directed downstream to the relevant portfolio company, or wherever the additional capital is required.

Separately, short-term opportunistic investments emerge by their very nature on an unpredictable timetable, and are unlikely to coincide neatly with liquidity events elsewhere in the fund, such as portfolio disposals. A NAV facility can therefore supply the rapid-deployment capital a manager needs to act on attractive opportunities as they materialise, enabling investment decisions to be made on their merits and without reliance on the timing of prior realisations.

Uses for limited partners: Distinct in legal form but analogous in economic effect, lending secured against fund interests also serves as a valuable tool for LPs and individual investors seeking to manage the timing of their own capital allocation and maximise the opportunities available to them. Rather than crystallising a loss on a position that would prove profitable if given sufficient time, NAV-collateralised borrowing allows investors to preserve optionality. This also strengthens the alignment of incentives between LP and GP, enabling both sides of the relationship to make decisions about extending fund life or managing residual holdings without concern for knock-on effects on their broader investment programmes.

Case study: Supporting an individual investor

An individual investor in a private equity fund wished to pursue an unrelated real estate acquisition, using their fund interest as collateral. By combining the diversified asset base within the fund with a personal guarantee and additional repayment sources, it was possible to provide a seven-figure facility with a flexible two-year maturity, enabling the investor to act on the opportunity.

Conclusion

The examples above illustrate the substantial benefits that small and mid-sized funds can realise through the optionality afforded by fund-level secured lending. In each instance, NAV facilities enhanced the borrower's control over the timing of key decisions and delivered the flexibility required to optimise investment outcomes. Free from institutional or administrative pressure to return capital or secure alternative financing, the GP is empowered to focus on maximising the economics of each investment.

A NAV lender that prioritises execution speed and adopts a genuinely collaborative approach with borrowers can significantly enhance the utility of such facilities while streamlining the overall process. Borrowers frequently require both decisive commitment and rapid turnaround from their lending counterpart in precisely the situations where a NAV loan would yield the greatest benefit—yet these are often the scenarios that present collateral characteristics or structural complexity falling outside the parameters of traditional bank lenders.

Having committed capital already in place is a critical advantage, particularly when combined with the experience and capability to execute thorough due diligence within a compressed timeframe. Private lenders typically encounter fewer institutional impediments to decision-making, with investment committees convening on short notice and individuals bearing direct accountability for outcomes rather than navigating layers of procedural documentation.

Nodem Capital is positioned to maximise these advantages through an exceptionally high degree of flexibility and responsiveness, enabling it to serve small and mid-sized borrowers, including on transaction sizes that larger private lenders may decline as insufficiently accretive to their return targets.

About Nodem Capital

Nodem Capital is a specialist NAV lending firm providing flexible, fund-level financing secured against portfolio value rather than individual portfolio companies. Purpose-built to serve small and mid-market fund managers, family offices, and private equity sponsors, Nodem delivers rapid, customised lending solutions with committed capital already in place. The firm's streamlined approach and deep structuring expertise enable it to act decisively on transactions that fall outside the parameters of larger institutional lenders.

1 Per Ares Partners' report, "The Evolution of Fund Finance", October 2024

2 ibid