Part 2 – Evaluating stress scenarios

NAV loans under stress

Part 2 – Evaluating NAV loan stress scenarios

Disclaimer: The model is illustrative to simplify the key mechanics. Holding periods are fixed, and performance fees have been excluded. The legal consequences of triggering covenants, whilst discussed, are absent from the models.

In Part 1, the Nodem team outlined the terms, mathematics, and logic behind fund-level NAV facilities. The case study was applied to a Growth fund looking to use the facility for follow-on investments.

You can read Part 1 here

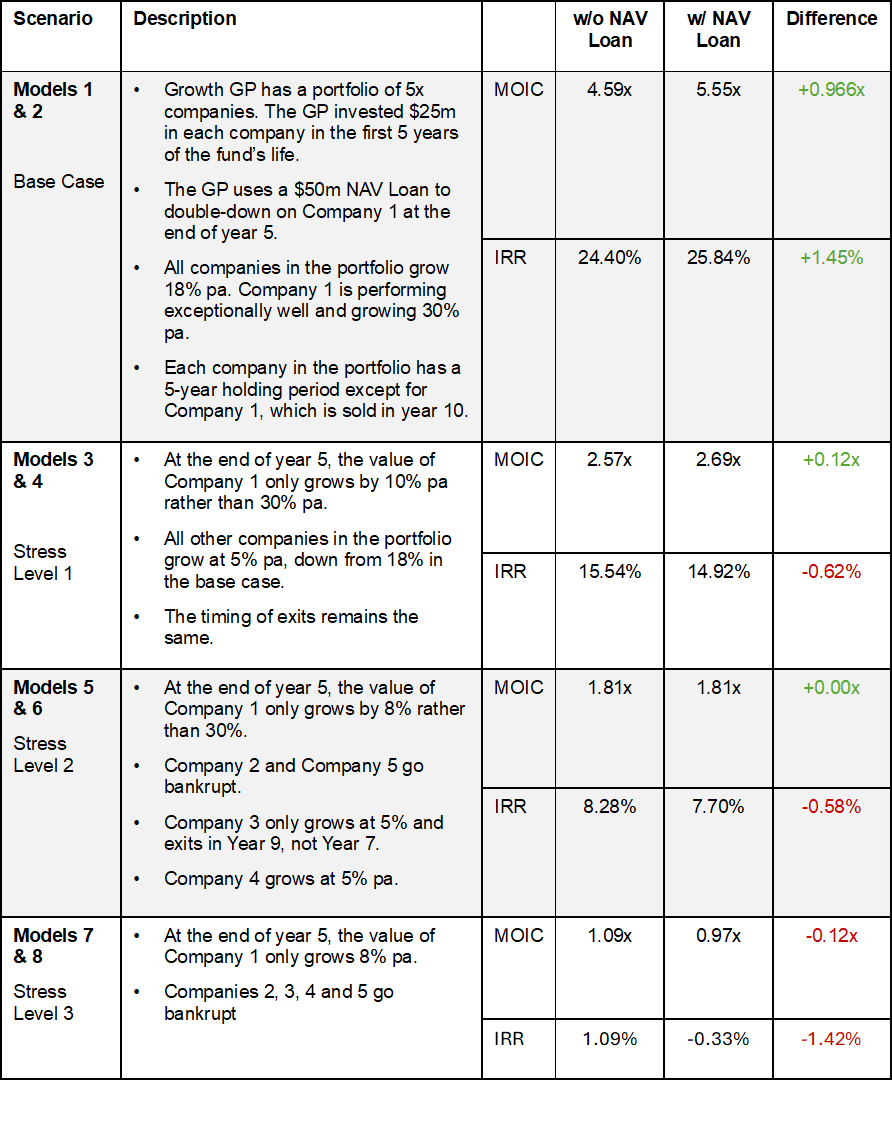

In Part 2, we run four scenarios focused on returns, with and without NAV facilities, across varying levels of stress. The goal of this series is for LPs and GPs to understand upside and downside scenarios. Part 3 will go deeper into structures/terms.

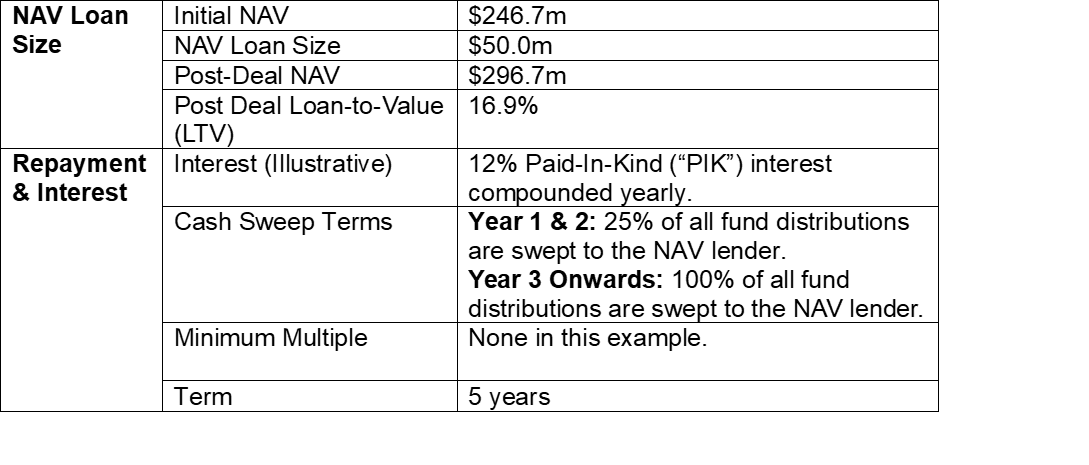

NAV Loan Terms (Illustrative) are the same for each scenario

Notes before moving to the worked models

Get in touch with Nodem to run through the model in detail. Here we present a simple worked mathematical illustration.

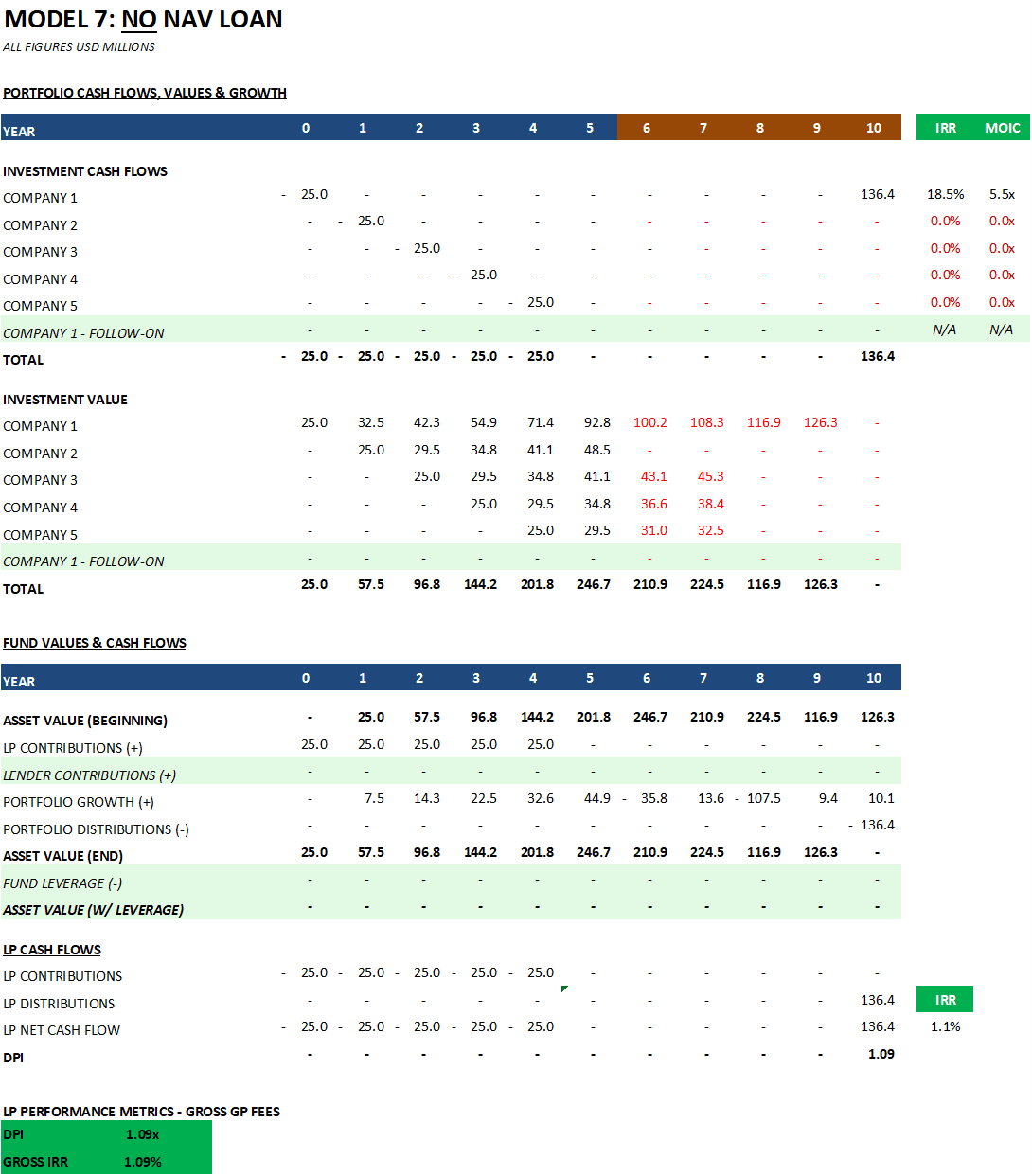

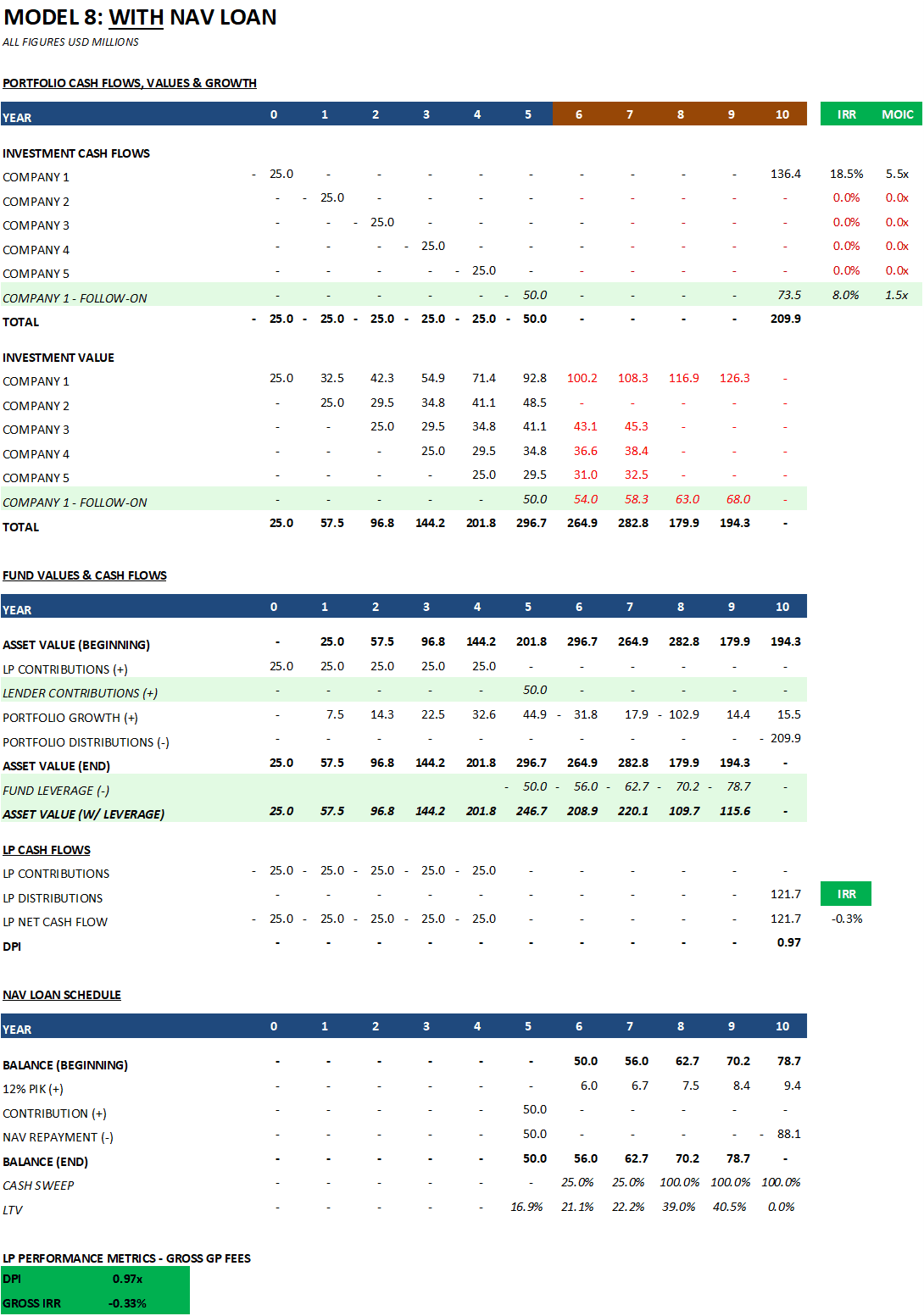

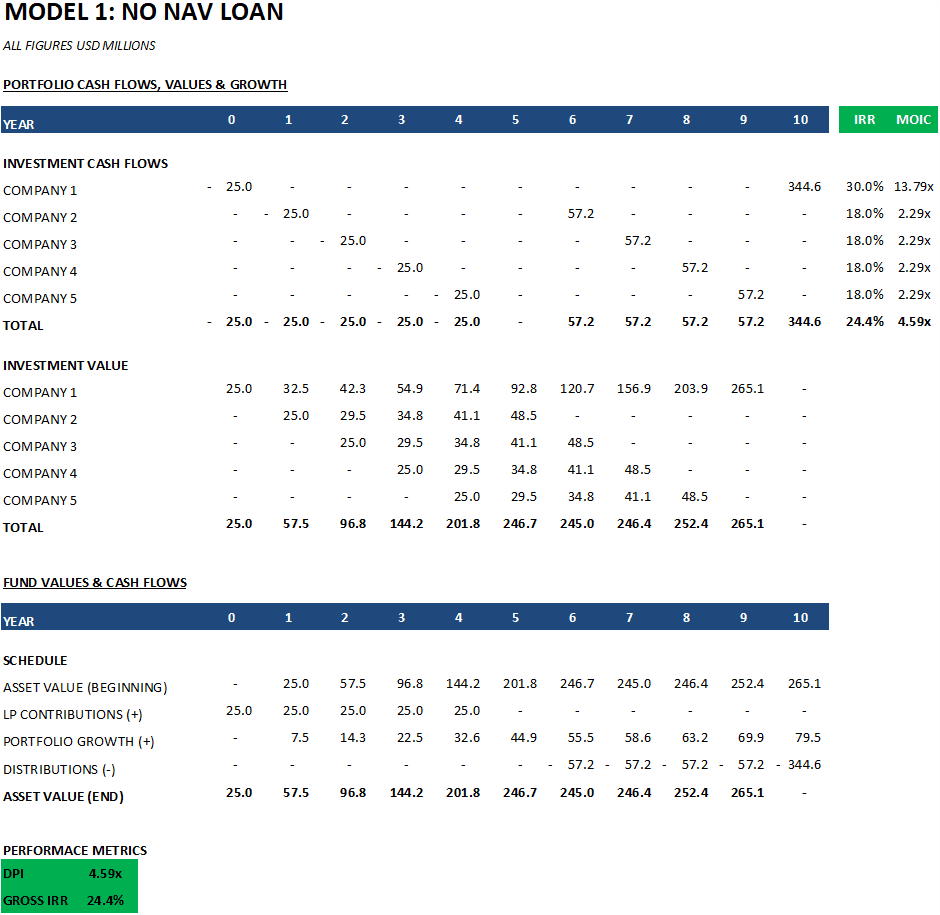

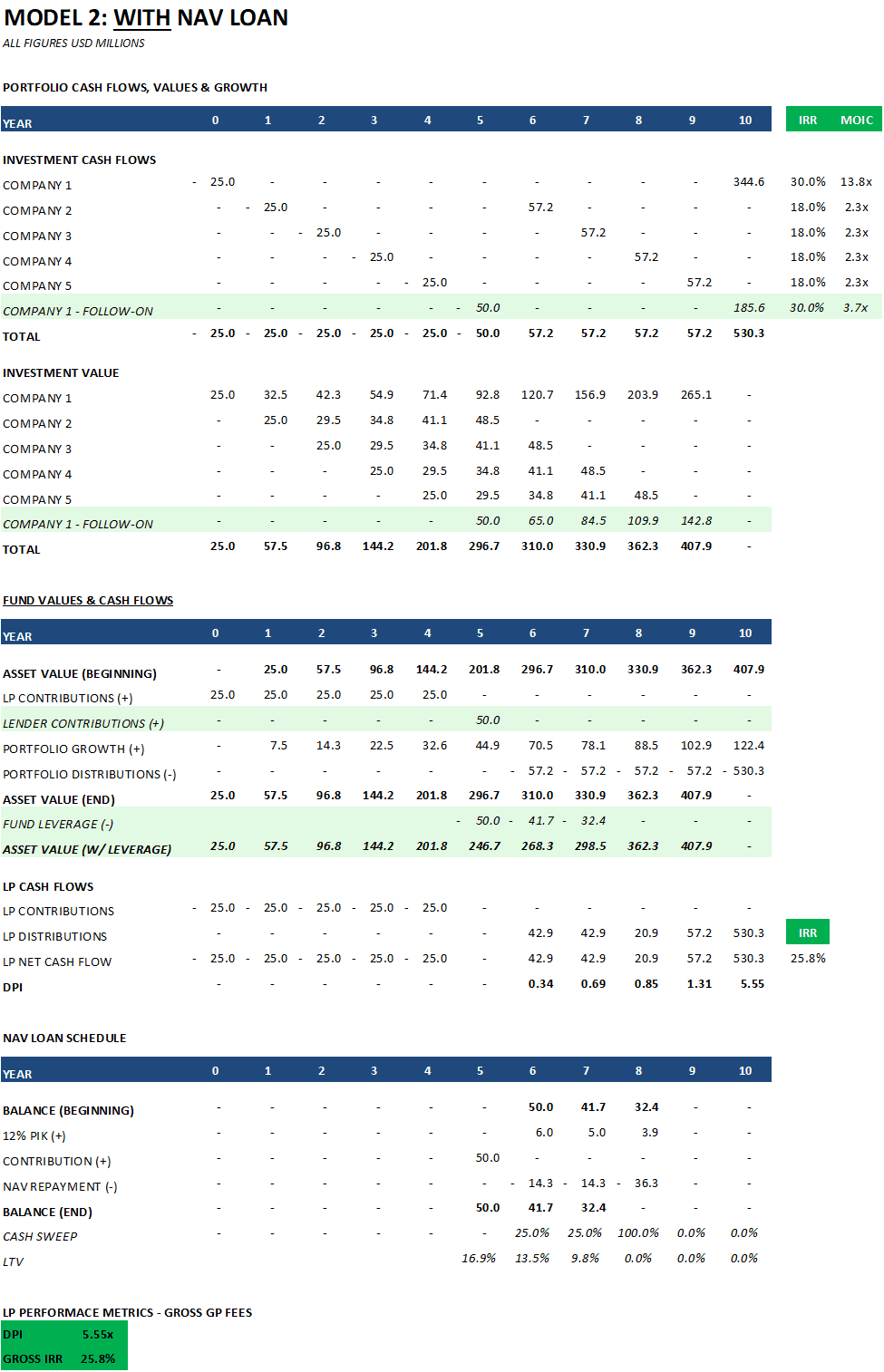

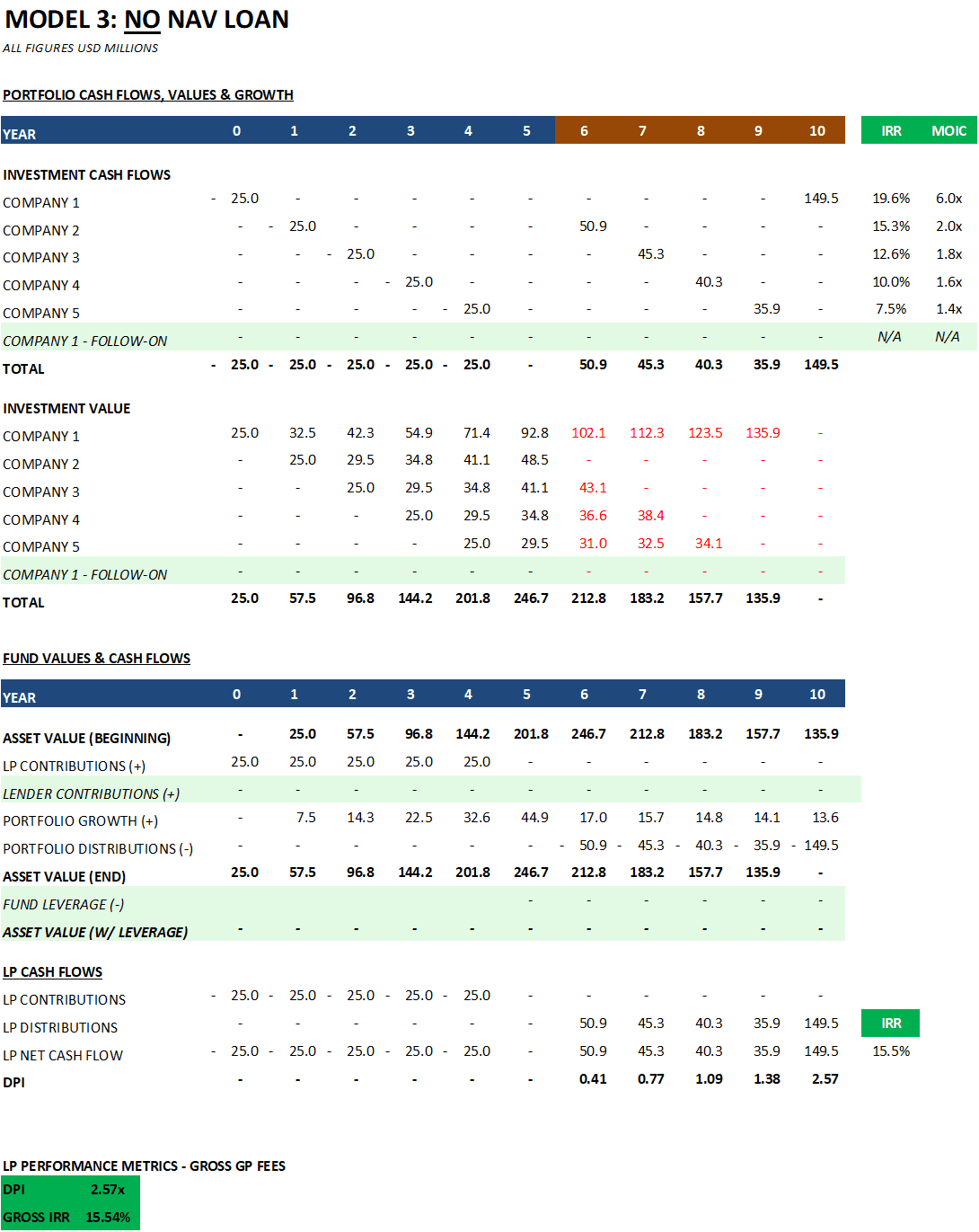

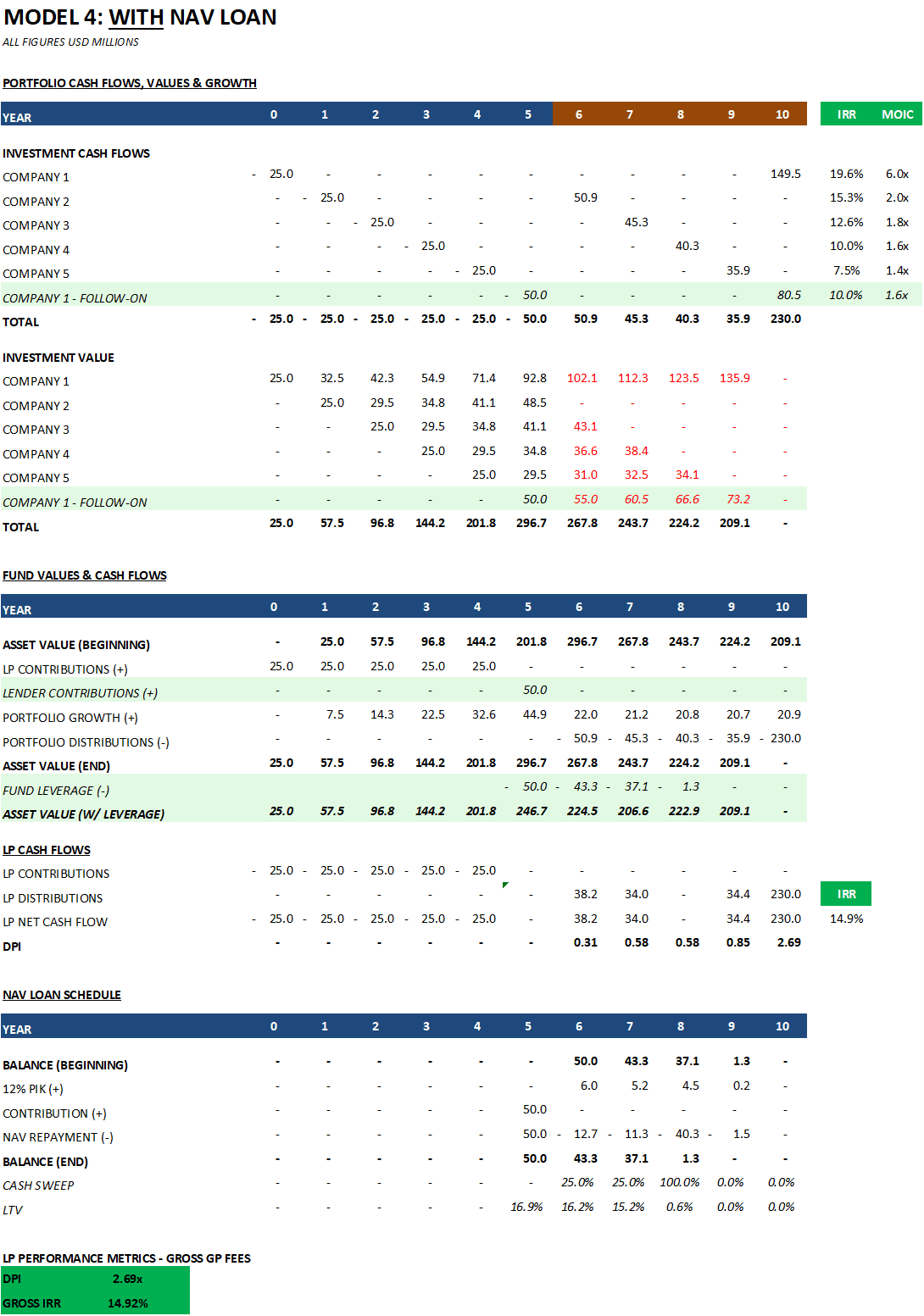

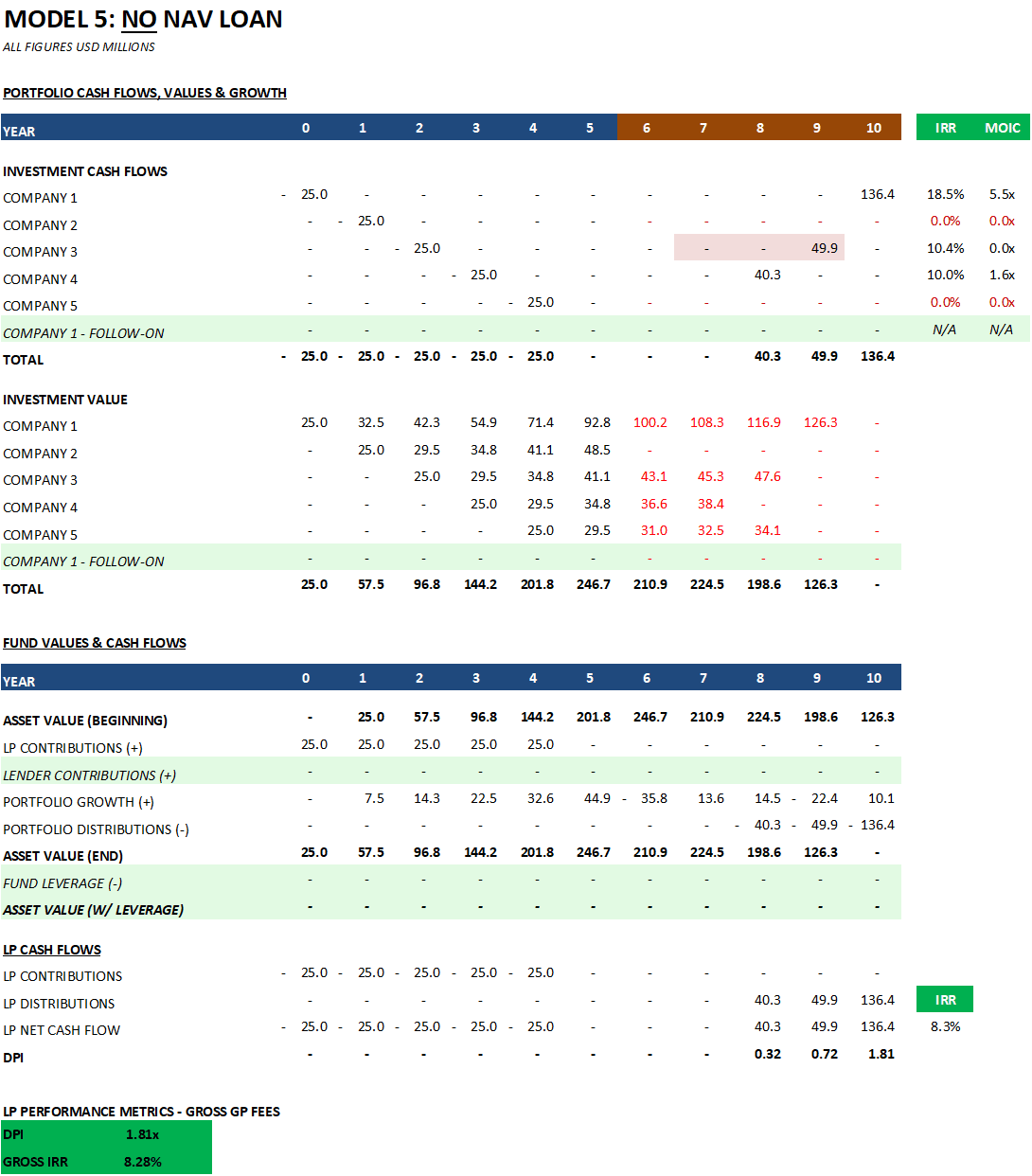

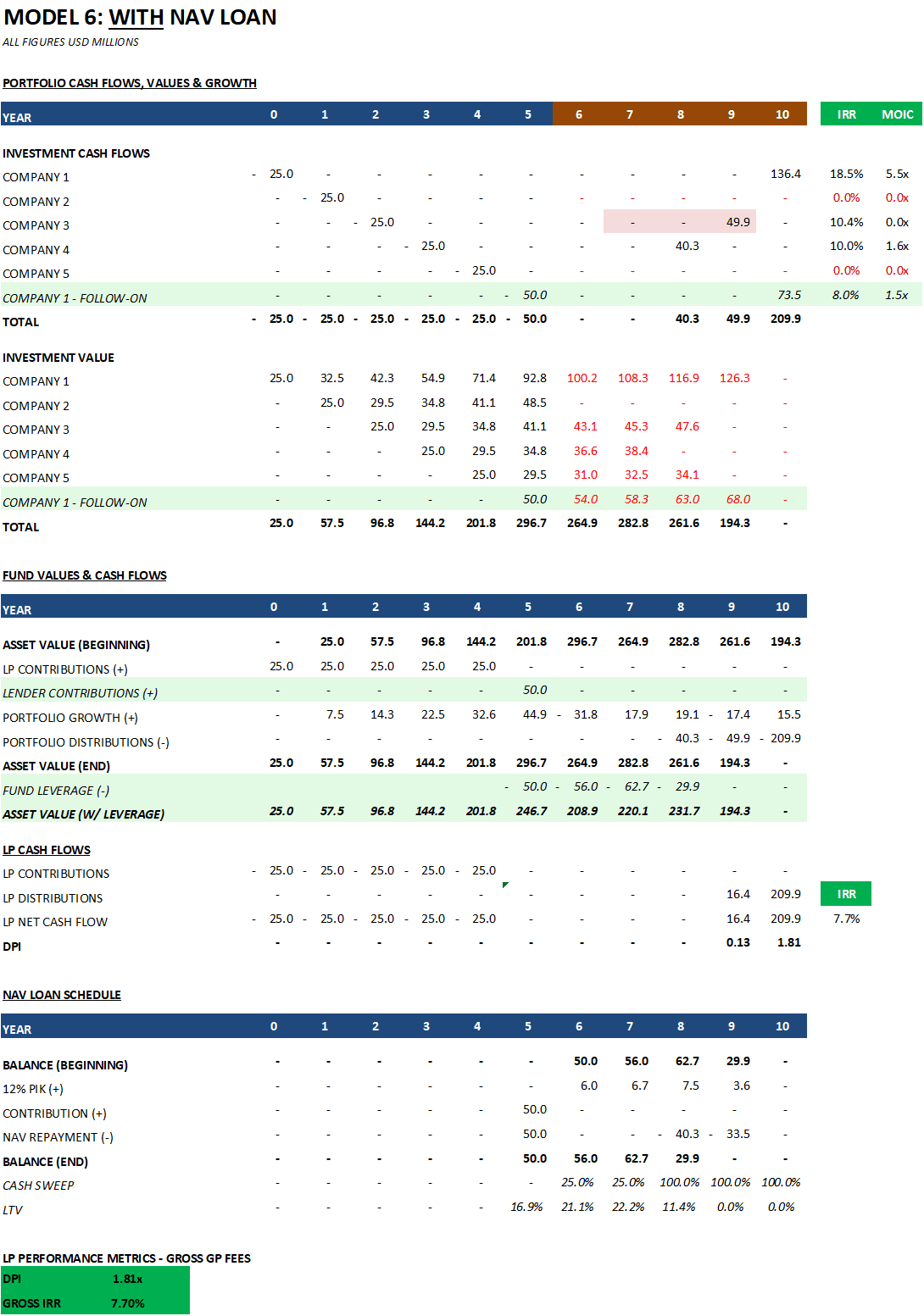

Portfolio Company Values: Details the timing of investments and divestments, company valuations over time, and growth rates. Investment cash flows, multiples, and timing align with the aforementioned portfolio metrics.

Fund Values and Cash Flows: Details the fund’s asset value, along with fund-level cash flows.

MOICs and IRRs under stress:

It is possible for a NAV loan to remain accretive even if the PIK exceeds the underlying investment return, IF the facility is repaid and the portfolio continues to grow.

IRRs are highly sensitive to cash flows. The MOIC can be positive while the IRR is negative, and vice versa. LPs should look at multiple return metrics.

This analysis ignores the legal consequences of triggering covenants, which can be significant. We will cover these in Part 3. However, as you read, keep the following in mind. If an LTV covenant (e.g., 2x starting LTV) or a time-based covenant (5yrs) is triggered, there are typically a few options after a cure period: refinancing or extending the facility. Eventually, a forced asset sale could be the fallback. GP capital contributions or LP recall are theoretically possible but rare and contentious. Some LPA provisions allow the GP to recall previously distributed capital, but exercising this right damages LP relationships and is seen as a last resort. The practical reality is that NAV lenders also don't want to foreclose on a portfolio - they'd end up owning minority stakes in private companies they have no ability to manage. This is why the cash sweep mechanism in the model matters so much - it amortises the loan using interim portfolio exits, reducing the risk of a large balloon payment at maturity.

BASE CASE

STRESS LEVEL 1

STRESS LEVEL 2

STRESS LEVEL 3