The mechanics of an accretive NAV financing scenario (PART 1)

Part 1 – Modelling LP returns with and without NAV financing

The mechanics of an accretive NAV financing scenario (PART 1)

Part 1 – Modelling LP returns with and without NAV financing

Part 2 - Evaluating scenarios and mitigating risks

Part 3 - Conclusions for strategic growth

Disclaimer: The model is illustrative to simplify the key mechanics. Holding periods are fixed, and performance fees have been excluded.

MODELLING LP RETURNS WITH AND WITHOUT A NAV FINANCING

In this article, the Nodem team outlines the terms, mathematics, and logic behind fund-level NAV facilities. Here applied to a Growth fund looking to use the facility for follow-on investments. The model is illustrative to simplify the key mechanics. Holding periods are fixed, and performance fees have been excluded.

Introducing NAV financing

NAV loans function as subordinated debt[1] secured by a private markets fund or a specific portfolio subset. Unlike traditional direct-to-company financing, the fund itself serves as the primary borrower.

While buyout funds have long utilized dividend recapitalizations to return capital, a NAV loan for distribution follows the same "re-levering" logic. The primary distinction lies in the application of leverage at the fund level rather than the asset level.

Three common use cases for NAV loans:

Accretive Investments: GP can buy more of a standout portfolio winner. NAV loans are a non-dilutive[2] capital that can be used to double down on winners.

Portfolio company distress: a GP needs fast rescue capital for a portfolio company or risk the loss of a significant portion of the portfolio's value.

Fund-level “dividend recap”: Take out a loan to fund LP distributions rather than doing so at the underlying portfolio level.

A Growth fund decides to use a NAV facility for an accretive investment

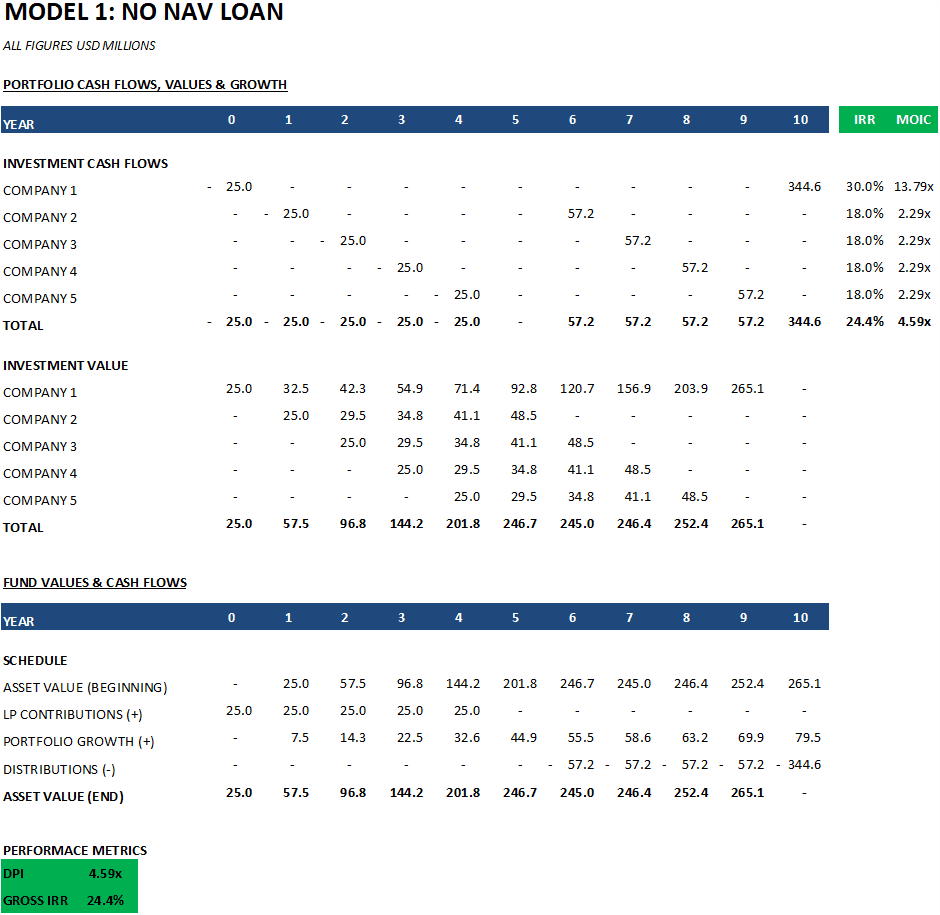

For simplicity, let’s assume a Growth GP has a portfolio of 5 companies. The GP invested $25m in each company in the first 5 years of the fund’s life.

The GP is now seeking a $50m NAV Loan to double-down on Company 1 at the end of year 5.

All companies in the portfolio have performed well, generating a 18% IRR. Company 1 is performing exceptionally well at a 30% IRR. The GP expects this strong growth to continue until a sale. A solid accretive use-case for a NAV loan.

Each company in the portfolio has a 5-year holding period except for Company 1, which is sold in year 10.

Why is the Growth GP considering a NAV facility?

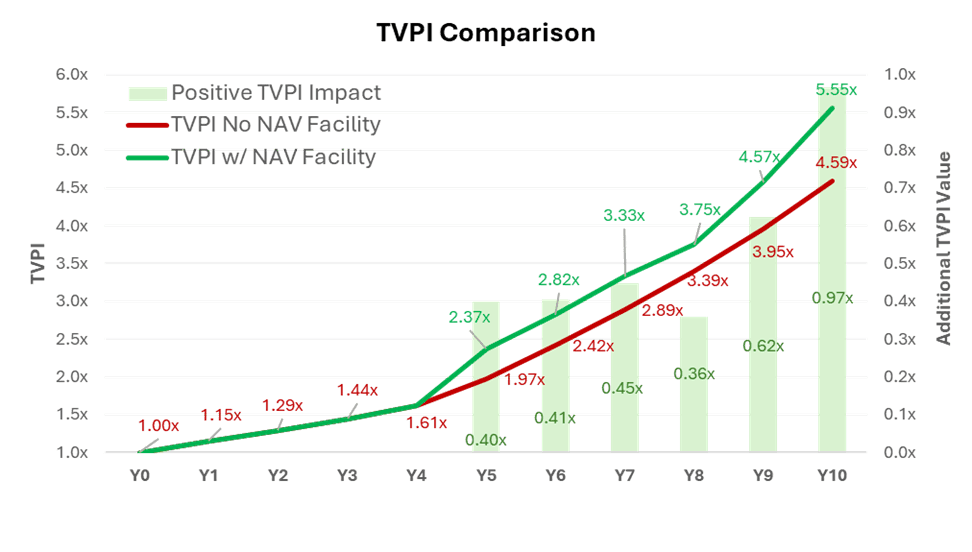

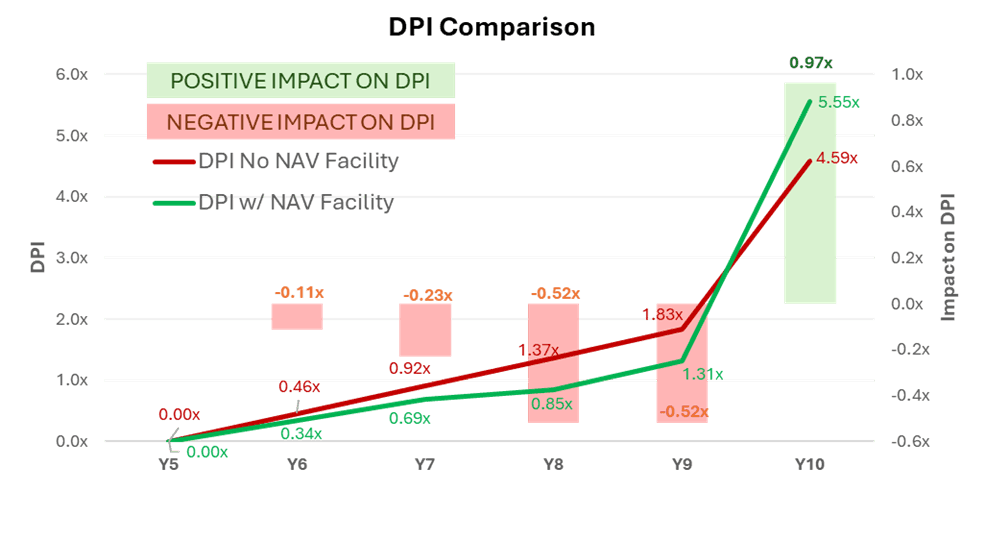

In the NAV Loan scenario, an additional $50m is invested in Company 1 in Year 5. In the scenario of not using a NAV Loan, there is no investment. All growth rates, holding periods, entries and exits, and MOICs are the same.

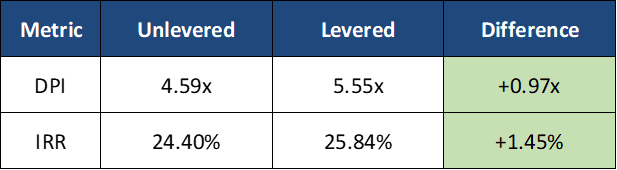

The models below run through the math, but let’s begin with the Growth GP’s estimation of the difference between using a NAV facility and not. The mathematical proof follows this section.

The GP calculates that the IRR and MOICs are likely to increase with a NAV loan in exchange for delayed distributions.

MODEL 1: THE GROWTH FUND WITHOUT A NAV LOAN

Get in touch with Nodem to run through the model in detail. Here we present a simple worked mathematical illustration.

Portfolio Company Values: Details the timing of investments and divestments, company valuations over time, and growth rates. Investment cash flows, multiples, and timing align with the aforementioned portfolio metrics.

Fund Values and Cash Flows: Details the fund’s asset value, along with fund-level cash flows.

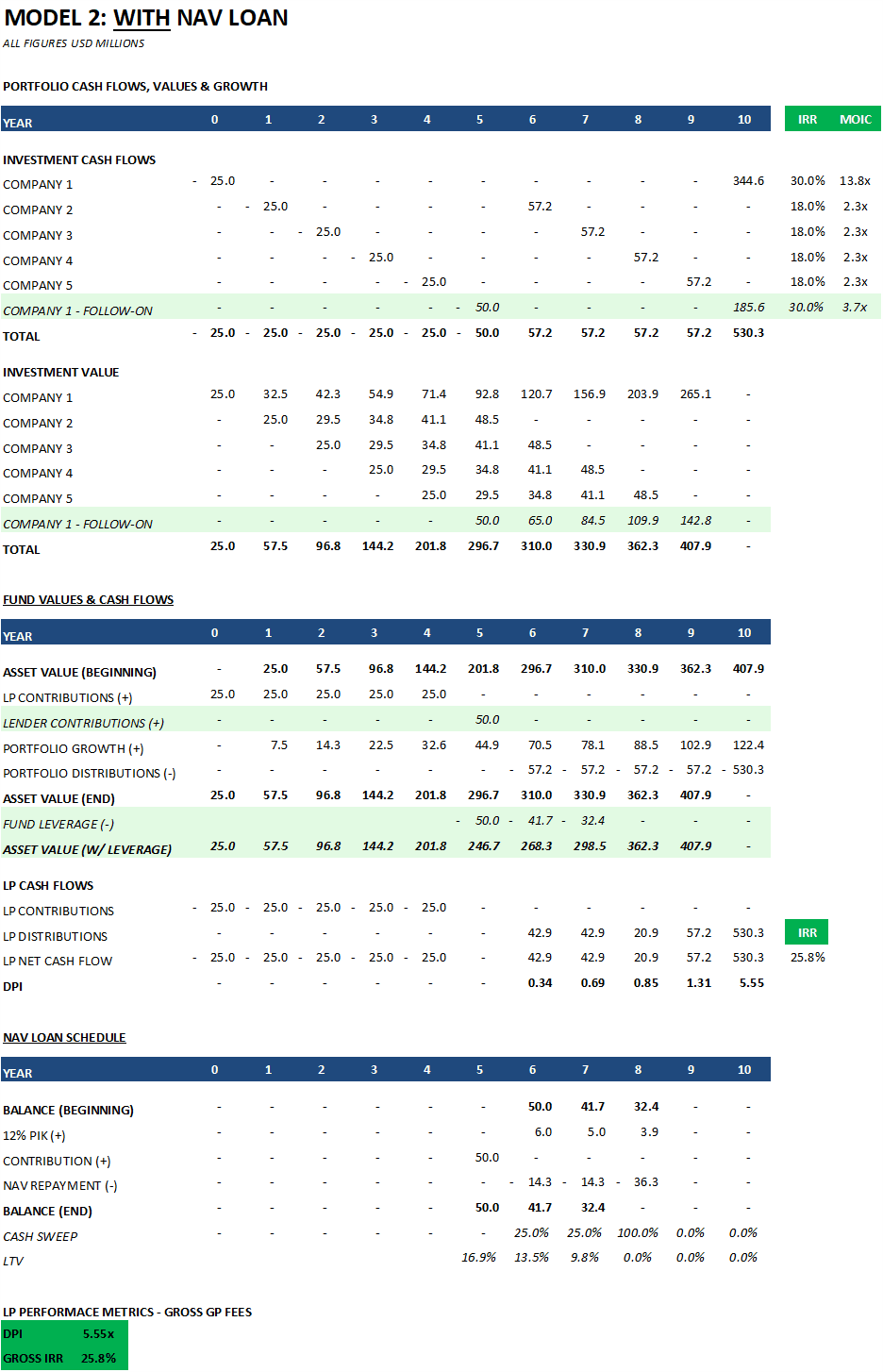

MODEL 2: THE GROWTH FUND WITH A NAV LOAN

Portfolio Company Values: Details the timing of investments and divestments, company valuations over time, and growth rates. Investment cash flows, multiples, and timing align with the aforementioned portfolio metrics.

Fund Values and Cash Flows: Details the fund’s asset value, including leverage from the NAV Loan, along with fund-level cash flows.

NAV Loan Debt Schedule: Details the NAV Loan’s debt schedule, including fund LTV, cash sweep assumptions, and the interest rate.

NAV Loan Terms (Illustrative)

NAV Loan Size | Initial NAV | $246.7m |

NAV Loan Size | $50.0m | |

Post-Deal NAV | $296.7m | |

Post Deal Loan-to-Value (LTV) | 16.9% | |

Repayment & Interest | Interest

| 12% Paid-In-Kind (“PIK”) interest compounded yearly. |

Cash Sweep Terms

| Year 1 & 2: 25% of all fund distributions are swept to the NAV lender. Year 3 Onwards: 100% of all fund distributions are swept to the NAV lender. | |

Minimum Multiple

| None in this example. |

Next week, we will post Part 2: Evaluating scenarios and mitigating risks. In the meantime, please reach out via the website to discuss in more detail.

[1] To avoid confusing a potential borrower, rephrase this to: "NAV loans are structurally subordinated to asset-level debt but sit senior to LP equity at the fund level.

[2] NAV loans provide non-dilutive capital that is accretive when the underlying asset's growth exceeds the cost of the facility.