Expensive compared to what?

Why a NAV loan at 700 over can be the cheapest capital a portfolio of private assets will ever raise.

The first reaction to NAV loan pricing is almost always the same. A spread of 700 basis points over a reference rate puts the all-in coupon at around 11% in today's market. For an investor used to thinking about senior bank debt, that number looks expensive. It is the wrong comparison.

A NAV loan is not competing with bank debt. Banks do not lend against portfolios of private assets at meaningful advance rates. The real alternative, the route that is genuinely available when a holder of private assets needs liquidity, is selling part of the portfolio in the secondary market. Once you put the NAV loan next to a sale at a realistic clearing price, the picture changes completely.

A worked example

Take a holding company or family office with a $100m portfolio of private assets compounding at 20% a year. The owner needs $25m, perhaps for a new commitment, a buyout of a partner, or simply to stop forced selling elsewhere. There are two ways to get it.

Borrow it. A NAV loan of $25m at a reference rate plus 700 basis points, roughly 11% all in, secured against the portfolio at 25% loan to value. The owner keeps 100% of the assets and 100% of the growth.

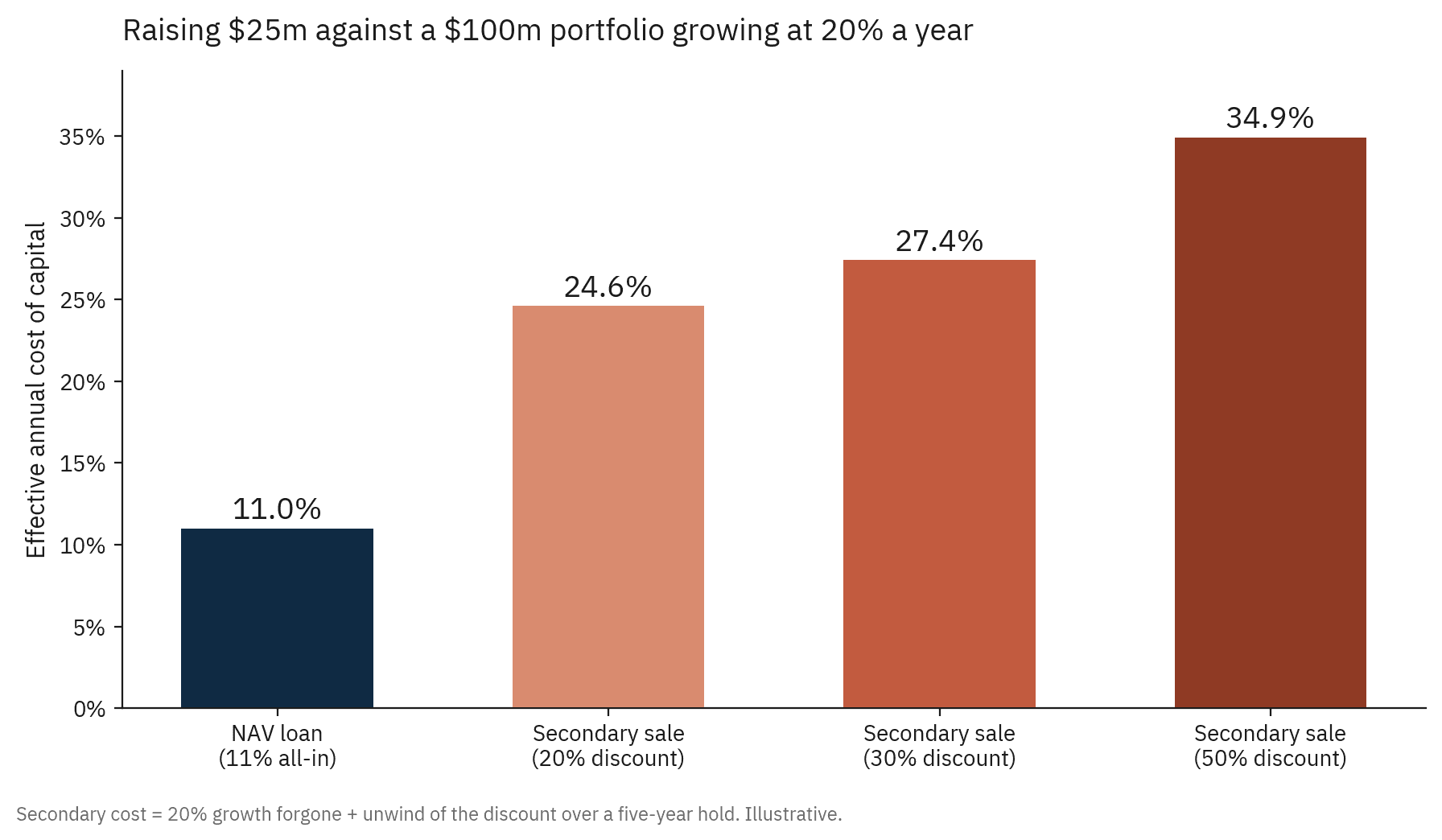

Sell for it. Private assets do not trade at par. Depending on the asset, the structure and the urgency, realistic clearing prices sit anywhere from a 20% discount to net asset value down to 50% for the hardest sales. The mechanics are unforgiving. To net $25m at a 20% discount, the owner has to part with $31.25m of NAV. At a 30% discount, $35.7m. At a 50% discount, a full $50m of NAV walks out the door to raise half that amount in cash. And the discount is only the visible part of the cost.

The hidden cost of selling a growing asset

The secondary route is the one that feels cheapest. No coupon, no covenants, no repayment date. But the cost of selling is the return you hand to the buyer, and for a growing asset that return is large.

Basic valuation theory makes the point. The value of a growing cash flow stream is its cash flow divided by r minus g, where r is the discount rate and g is the growth rate. The multiple 1/(r-g) is exquisitely sensitive to growth. An asset growing at 20% against a 25% discount rate is worth 20 times its cash flow. Strip the growth out and it is worth 4 times. Almost all of the value in a compounding asset sits in its future, not its present.

When you sell, you sell the future with it. The buyer earns two returns: the 20% the asset compounds at anyway, plus the unwind of the discount as the position pulls back towards fair value over their hold. Over five years, a 20% discount adds roughly 4.6% a year, a 30% discount 7.4%, a 50% discount nearly 15%. The buyer's expected return is the seller's cost of capital. Raising $25m by selling therefore costs roughly 24.6% a year at a 20% discount, 27.4% at 30%, and 34.9% at 50%. The 11% loan is less than half the cost of even the best secondary outcome.

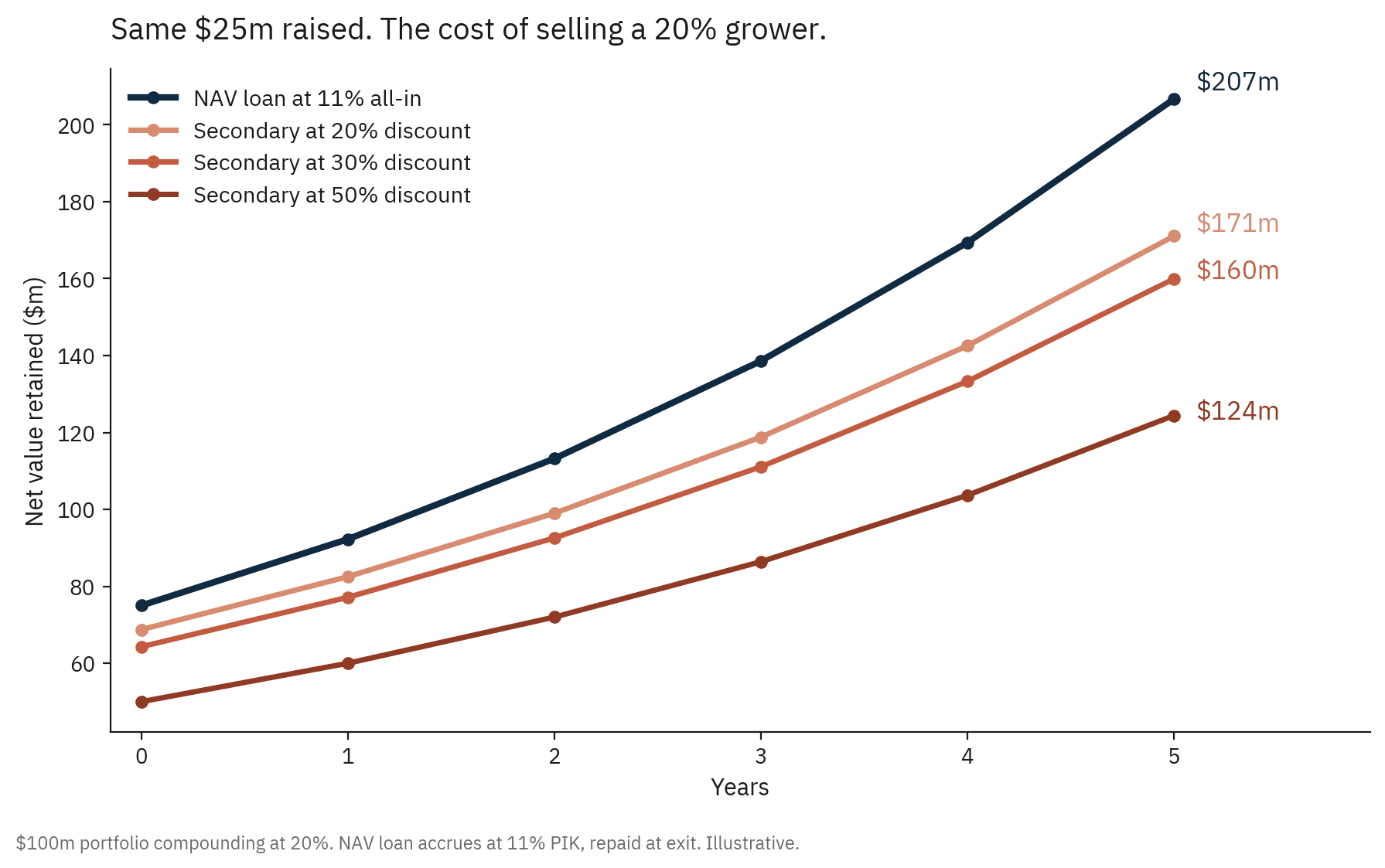

Run it forward five years. With the loan, the portfolio compounds to $249m and the loan balance grows to $42m, a net position of $207m. Sell at a 20% discount and the retained NAV reaches $171m. At 30%, $160m. At 50%, $124m. Same $25m of liquidity in every case, and the gap between borrowing and a distressed sale is $82m, more than three times the original facility.

Five hard questions a sceptical CFO should ask

You have assumed 20% growth. Isn't the growth assumption doing all the work? Less than you would think. The break-even is what matters, and it is low. Against a sale at a 20% discount, the loan wins whenever the portfolio grows faster than 6.2% a year. Against a 30% discount, the hurdle is 3.4%. Against a 50% discount, the loan wins even if the portfolio shrinks by up to 3.4% a year, because handing over $50m of assets for $25m of cash is a hole that almost no outcome digs you out of. The case for borrowing does not require heroic growth. It requires believing your portfolio will do better than roughly flat.

If buyers will only pay 70 cents, isn't the market telling you NAV is overstated? Sometimes, and that deserves honesty. Part of any discount is price discovery on stale marks. But discounts on private assets persist even where marks are conservative, because buyers are pricing illiquidity, diligence cost and their own return hurdle, not just valuation doubt. The practical test is simple: if you believe the discount reflects your true value, sell. If you believe in the asset, the discount is a cost, not a correction, and borrowing against it is cheaper than donating it.

Doesn't selling de-risk while borrowing adds risk? Yes, and this is the most important objection. A sale converts paper into cash and ends the exposure. A loan keeps the full exposure and adds a fixed claim against it. The comparison in this piece is for owners who want to keep the asset. If the goal is to exit the risk, sell and accept the price. If the goal is liquidity without giving up an asset you believe in, the loan is the cheaper route, and the protection against being wrong is the advance rate. At 25% to 30% loan to value, the portfolio can fall by half before the lender's claim threatens the equity.

Is 11% really the all-in cost? Here, yes. The 11% used throughout this piece is the all-in number, the spread over the reference rate with arrangement fees and costs amortised over the life of the facility. That is the figure any borrower should insist on seeing, because a clean headline coupon with fees layered behind it is how cheap money becomes expensive. What still deserves diligence is structure rather than price: LTV covenants and cure mechanics, where conservative initial leverage is what keeps the pressure remote. Even so, the gap to the cheapest secondary outcome is more than thirteen points a year.

Debt has a maturity. What if the exit slips? A fair point, and the reason tenor matters. A sale is final; a loan must be repaid or refinanced. The discipline is to size the facility against a realistic exit timeline with headroom, and to keep leverage low enough that refinancing is a pricing question rather than an existential one. A 25% LTV facility on a performing portfolio refinances. What does not come back is the $25m of value surrendered on day one of a discounted sale.

Nodem Capital provides portfolio-backed NAV facilities of $20m to $100m+ to family offices, GPs, LPs and investment holding companies, at up to 30% loan to value.