How are sponsors using NAV loans?

A lender-focused guide to NAV lending, covering market growth, sponsor use cases, structural protections, underwriting priorities, and recreated market visuals.

NAV lending has evolved from a specialist financing tool into a mainstream part of private markets capital formation. In an environment where exits have taken longer, distributions have slowed, and sponsors have needed more flexibility around mature portfolios, fund-level loans backed by portfolio assets have become an increasingly important source of liquidity and strategic optionality.

For lenders, the attraction is straightforward. NAV facilities are generally underwritten against a diversified pool of seasoned assets rather than a single operating company. That can create a more resilient collateral base, improve visibility into repayment, and support attractive risk-adjusted returns when leverage, structure, and sponsor quality are all aligned.

NAV loans tend to be at their best when they support value creation, prudent refinancing, or balance-sheet optimisation. They merit greater scrutiny when used primarily to accelerate distributions.

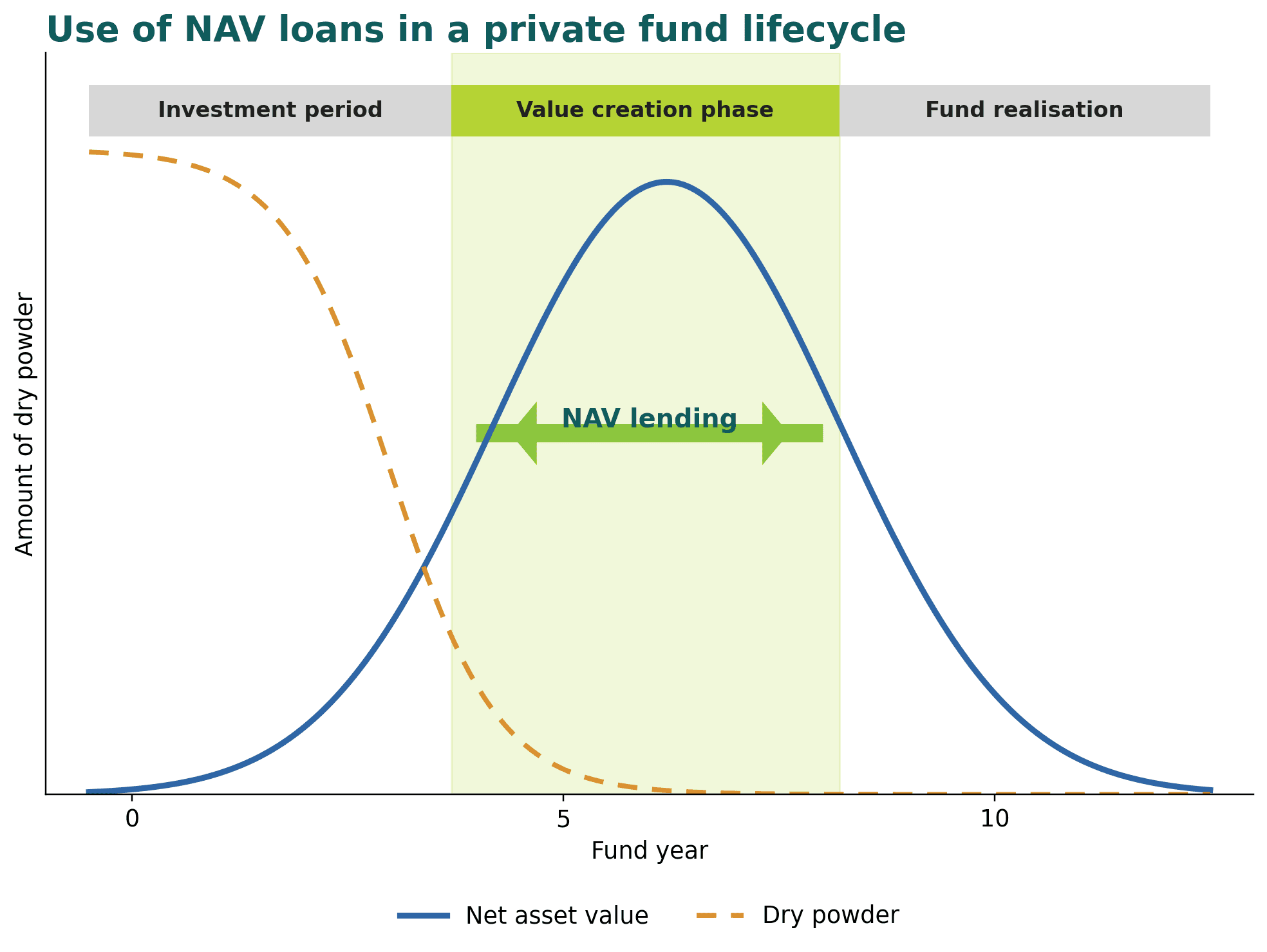

Why NAV lending has become more relevant

Private equity firms have spent the last several years navigating a difficult exit environment. Valuation expectations, financing costs, and buyer appetite have not always aligned, which has often forced sponsors to hold assets longer than expected. That has increased the need for financing tools that preserve flexibility without requiring an immediate exit at an unattractive valuation.

This environment has naturally favoured NAV lenders. Mature portfolios usually provide more operating history, more reliable reporting, and a clearer basis for underwriting enterprise value and potential realisation paths. The same market conditions that have created financing needs for sponsors have therefore also improved the information available to lenders.

What is NAV financing?

NAV financing is a form of fund-level lending in which repayment is underwritten against the value and cash flows of the fund’s underlying portfolio. Unlike subscription finance, which relies on uncalled LP commitments, NAV loans are secured against the assets themselves and are typically used later in the life of a fund, when embedded value has already accumulated.

Structures vary, but the market is commonly characterised by conservative opening leverage, medium-term maturities, and bespoke credit protections. The source article describes typical entry LTVs of around 10 to 20 per cent, loan tenors of three to five years, and facility sizes ranging from about $50 million to more than $1 billion, depending on portfolio size and quality.

Subscription lines and NAV loans are not interchangeable

Although both products sit within fund finance, they are designed for different stages of the fund lifecycle and depend on different underwriting disciplines.

Feature | Subscription lines | NAV loans |

Main collateral | Uncalled LP commitments | Underlying portfolio assets and related cash flows |

Typical timing | Early in the investment period | Later in the value-creation and harvest period |

Typical duration | Short term | Three to five years |

Main repayment source | Capital calls | Portfolio realisations, dividends, refinancings, or asset sales |

Core underwriting lens | Investor quality and commitment-based | Portfolio quality, concentration, valuation, and exit paths |

For NAV lenders, this distinction matters because the core task is not simply to assess the sponsor. It is to evaluate the portfolio's strength, diversification, and monetisation potential.

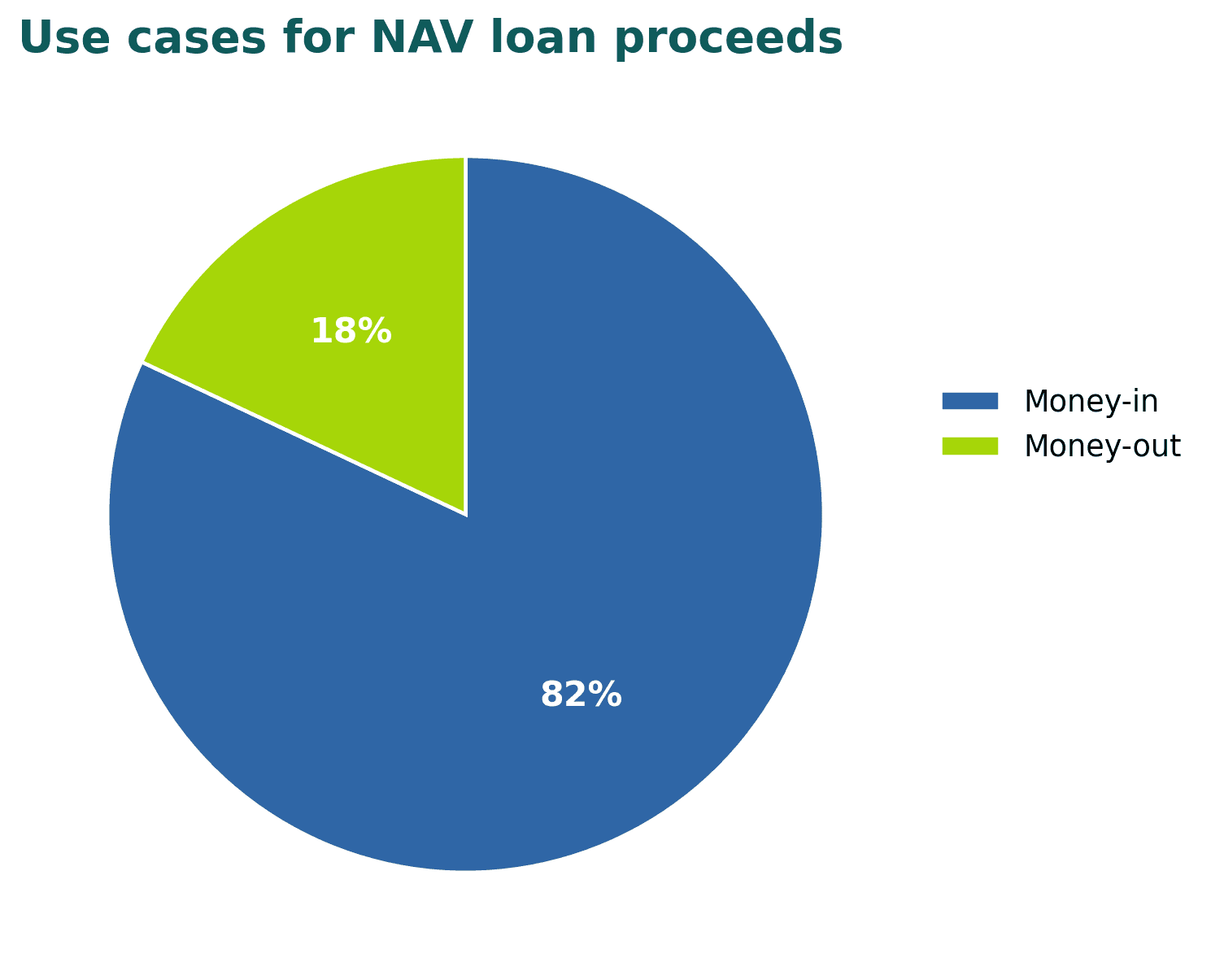

How sponsors use NAV loan proceeds

Sponsors usually use NAV facilities in three ways. The first is reinvestment, in which the proceeds are used for add-on acquisitions, portfolio-company growth, or working capital support. The second is refinancing, where a NAV facility replaces more expensive or more restrictive obligations. The third is distribution support, in which the loan is used to accelerate the return of liquidity to LPs without an immediate sale event.

From a lender’s perspective, the difference between these use cases is material. Reinvestment and refinancing can be constructive if they improve the value or resilience of the collateral pool. Distribution-led transactions are more controversial because they may improve headline distribution metrics without actually increasing enterprise value. That is why lenders often distinguish between so-called money-in and money-out deals.

Why lenders are attracted to the strategy

A strong NAV loan can sit in a favourable part of the private credit spectrum. A diversified collateral pool can reduce single-name risk, while structural protections such as cash-account control, concentration limits, covenants, and negotiated waterfalls can strengthen lender recoveries in downside scenarios.

The strategy can also complement a broader direct-lending programme. Traditional direct lending is usually built around loans to individual businesses. NAV finance introduces a different return driver, because repayment is linked to a pool of sponsor-backed assets and their monetisation over time. That makes the strategy a source of diversification rather than just another way to express the same credit risk.

Risks lenders should underwrite carefully

The benefits of diversification should not be overstated. A portfolio can appear diversified and still be vulnerable if a small number of assets account for most of the NAV, if several holdings share the same macro exposure, or if valuation marks are slow to reflect market reality. Concentration and correlation remain essential underwriting considerations.

Valuation discipline is equally important. Because NAV loans are underwritten against unrealised value, lenders need a clear sense of what the collateral could be worth not only in the base case, but also in a slower, weaker, or more selective exit environment. Downside analysis matters at least as much as sponsor marks.

Use of proceeds should also be treated as a core credit variable. A facility that supports portfolio growth may improve the lender’s position by strengthening the assets underlying the loan. A facility that withdraws liquidity from the structure too early may weaken repayment flexibility. The loan purpose is therefore not just a transaction detail; it is one of the main determinants of future risk.

A representative transaction profile

The source article includes a case study involving a $3 billion 2017-vintage fund seeking a $150 million first-lien NAV facility at roughly 5-10 per cent LTV, with proceeds earmarked for follow-on investment and working capital support. The broader significance of the example is structural. The loan combined moderate leverage with diversified collateral, a delayed-draw component, cash-control mechanics, waterfall protections, and portfolio-level covenants.

That is a useful reminder that attractive NAV loans are rarely defined by spread alone. What matters is how sponsor quality, asset quality, diversification, structure, and repayment logic fit together.

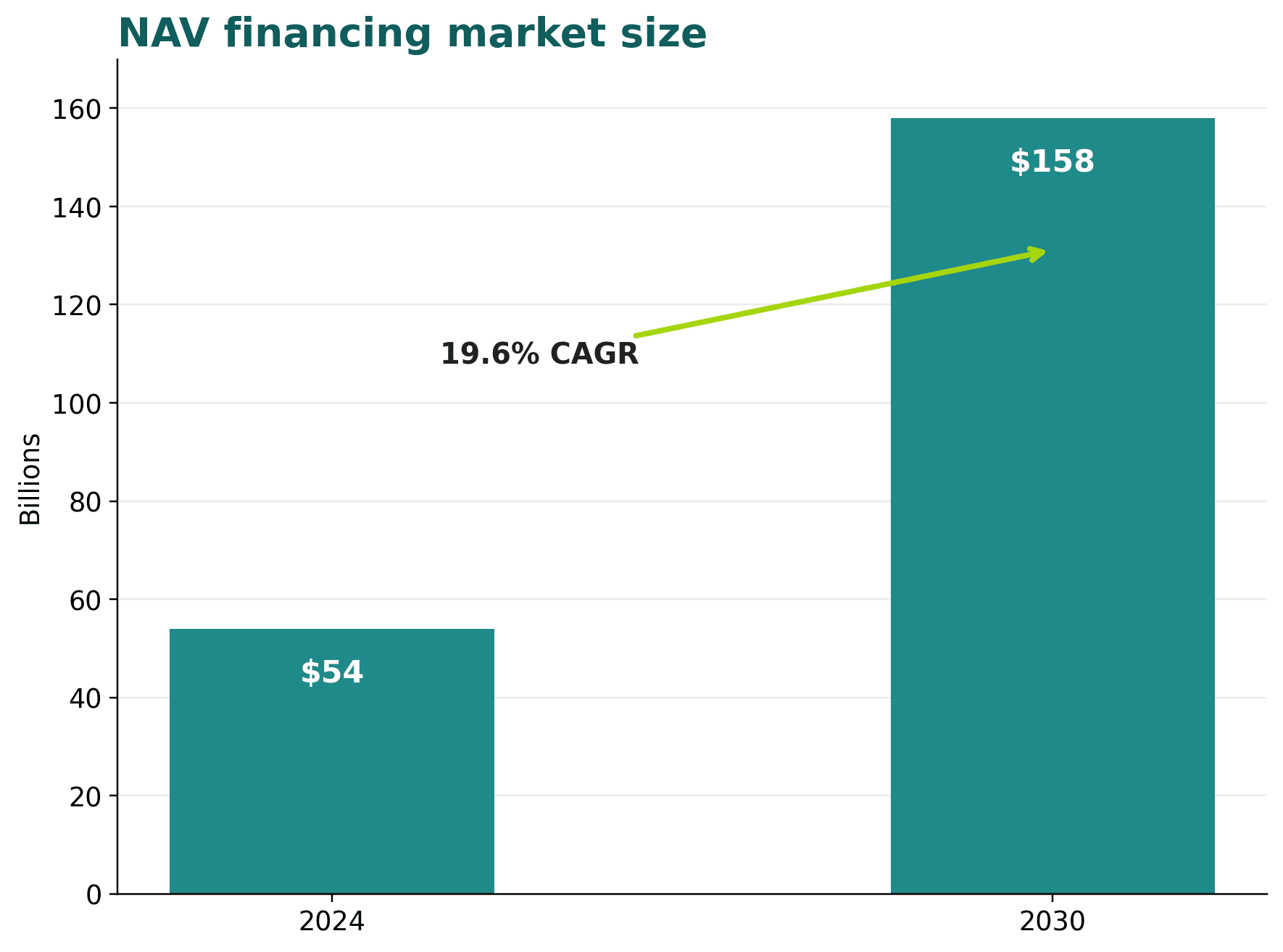

Market growth and the opportunity set

At the time of the source article, the NAV lending market was still viewed as small relative to the overall size of private equity, despite high growth expectations. That remains one of the strategy’s key attractions. The addressable market is large, but current penetration is still comparatively modest.

In the recreated market-size illustration, the market expands from $54 billion in 2024 to $158 billion by 2030, implying growth of just under 20 per cent per year. Those figures have been adjusted from the original source, but the strategic point remains the same: NAV finance still has significant room to scale if private markets continue to face slower exits, selective capital formation, and a need for more flexible portfolio-level solutions.

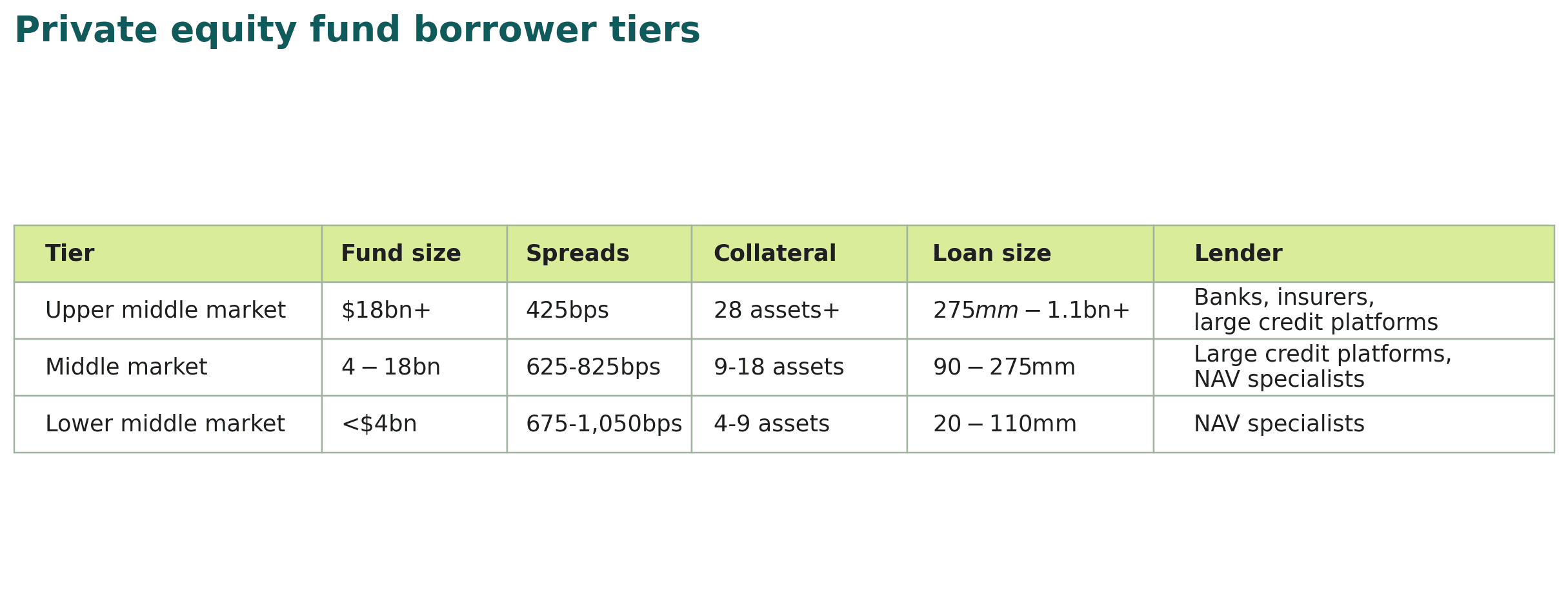

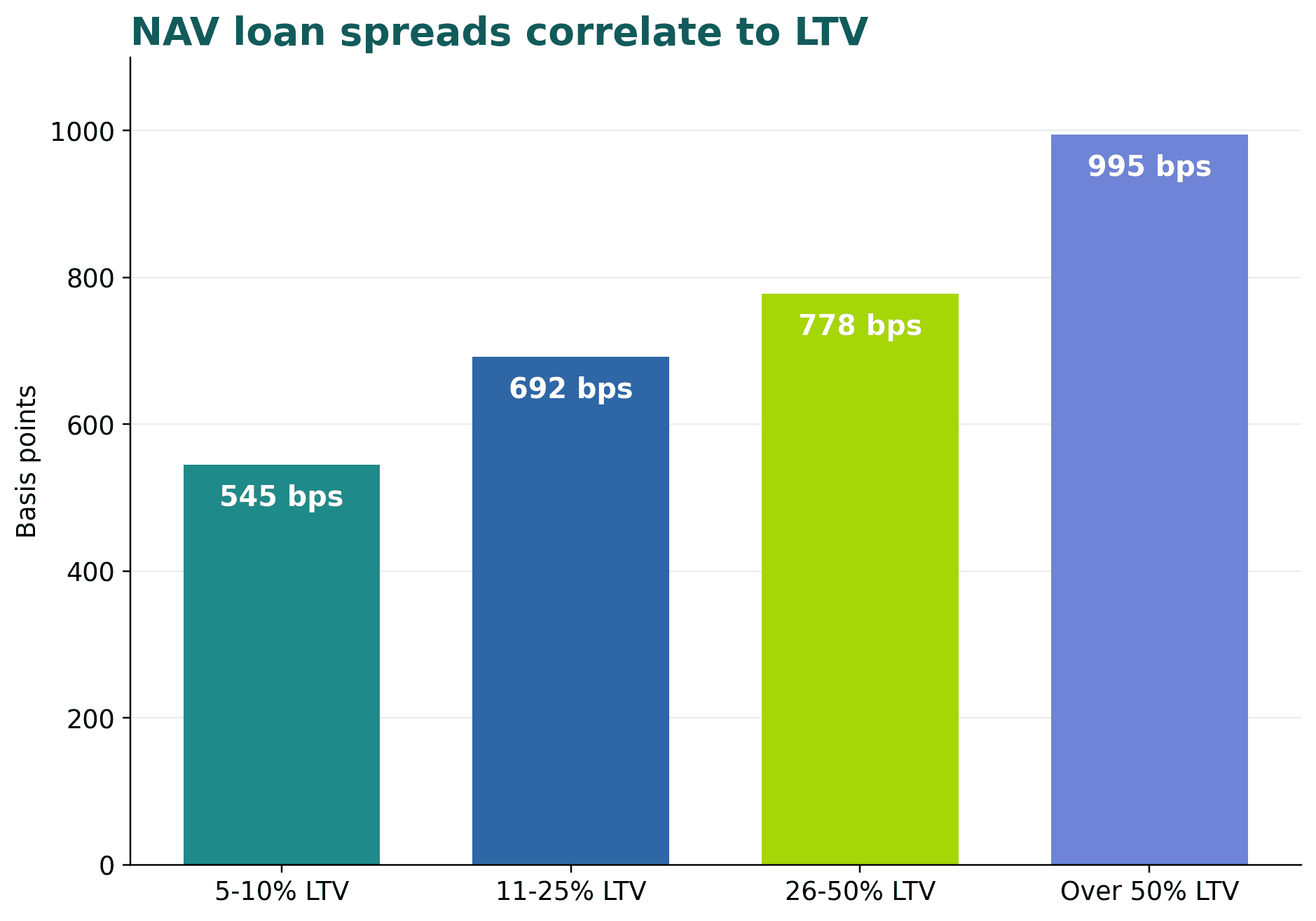

Borrower segmentation and pricing logic

Larger funds generally bring more diversification, more seasoned assets, and often better pricing. Smaller funds can still offer compelling opportunities, but they often require wider spreads and tighter structural protections because concentration and execution risk are typically higher.

The recreated borrower-tier table and spread-versus-LTV chart reflect the same broad market logic. As portfolio size and diversification decline, lender specialisation and spread expectations rise. As leverage increases, pricing should widen to reflect the reduced downside cushion.

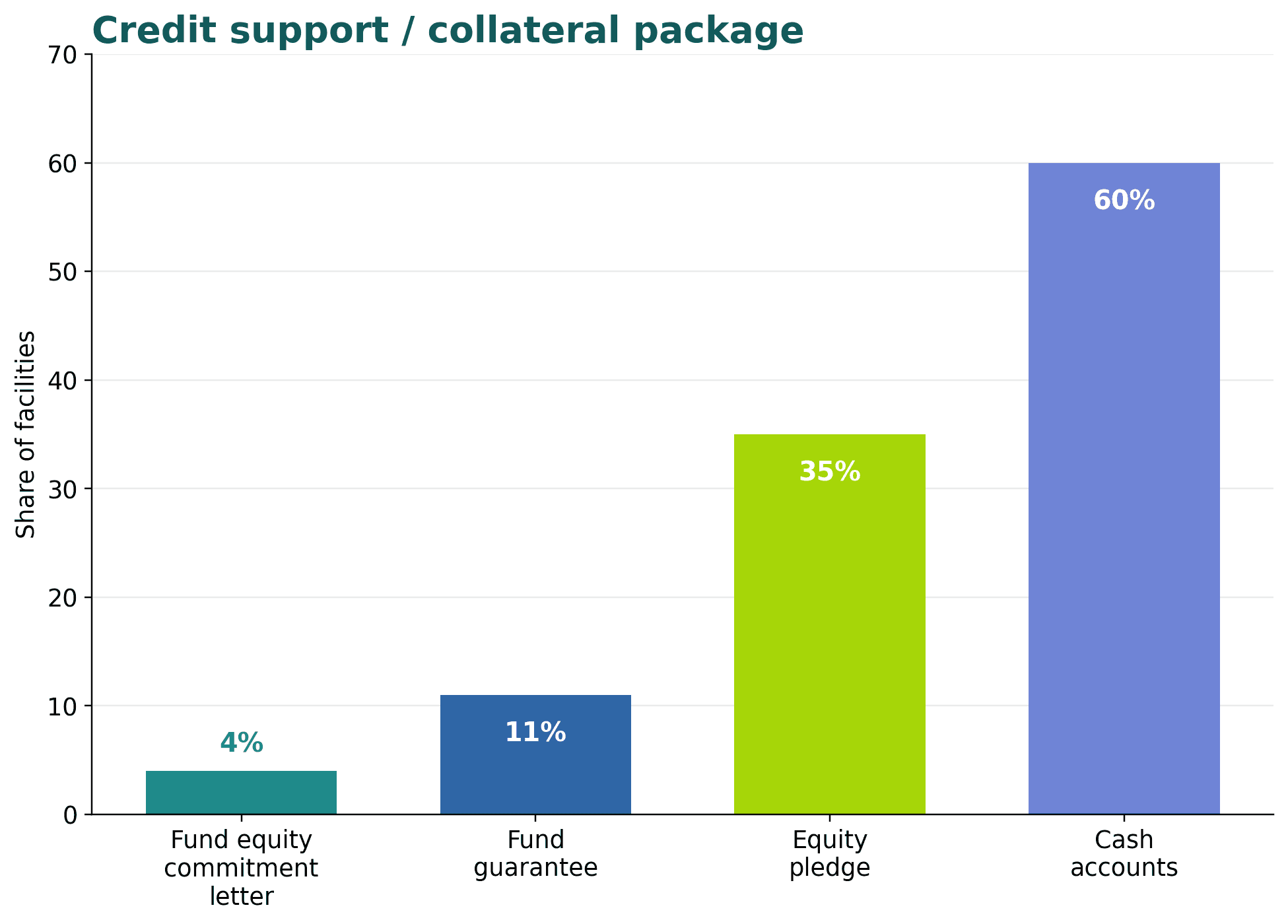

Structure remains decisive

The best NAV loans are not simply low-LTV loans. They are loans with coherent structures. Cash accounts, equity pledges, guarantees, concentration limits, NAV coverage tests, and waterfalls all influence how much real control a lender has if portfolio performance deteriorates.

The source article highlights cash-account control as the most common form of credit support in the market. The recreated collateral-support chart preserves that ordering while modestly adjusting the figures to keep the visual original.

What lenders should prioritise in underwriting

Underwriting area | Key question | Why it matters |

Sponsor quality | Does the GP have a strong track record in value creation and exits? | Sponsor behaviour and execution influence both collateral value and workout outcomes |

Portfolio concentration | How much NAV sits in the top positions and sectors? | Concentration weakens the benefits of diversification |

Asset quality | Are the underlying companies performing and financeable? | Weak assets reduce recovery value quickly |

Valuation discipline | Are marks supported by evidence and downside analysis? | Overstated NAV leads directly to mis-sized leverage |

Use of proceeds | Is the facility supporting value creation or extracting liquidity? | Loan purpose affects future flexibility and incentives |

Structure | Who controls cash, collateral, and reporting? | Structure determines real-world lender protection |

Exit path | What is the realistic route to repayment within tenor? | Repayment certainty matters more than headline NAV |

Conclusion

NAV lending is increasingly important because it solves a real problem in private markets: mature portfolios often need liquidity and flexibility before exits are ready. For lenders, the opportunity is attractive when it is backed by diversified assets, conservative leverage, robust structure, and a sponsor using the capital for the right reasons.

The opportunity is not uniform, however. The best lenders in the market will be the ones who stay selective, underwrite cash flow and realisation pathways rather than paper value alone, and treat governance, structure, and sponsor alignment as core components of the credit decision.