Is NAV Lending Asset-Backed Finance? Yes, But Not the Kind You Think

NAV facilities share the structural DNA of asset-backed lending. The risk drivers are entirely different. Understanding the distinction matters for anyone allocating to either.

Asset-backed finance has become one of the most crowded phrases in private credit. Managers raising ABF strategies, allocators building ABF sleeves, and conference agendas full of ABF panels all use the term to mean lending secured against pools of assets rather than corporate cash flows. NAV lending is increasingly grouped into this bucket. The grouping is defensible on structure and misleading on substance. This piece sets out what asset-backed lending normally means, where NAV facilities genuinely belong in that family, and where the analogy breaks down.

What people usually mean by asset-backed lending

When practitioners talk about asset-backed lending or asset-based finance, they typically describe credit secured against pools of contractual cash flows or hard assets, in which the collateral itself generates repayment. The classic universe includes trade receivables and invoice finance, inventory and borrowing-base facilities, equipment leasing, auto loans, consumer credit pools, royalties, aircraft, and the broader securitisation-adjacent world that private credit managers now market as speciality finance.

Four features define the category.

Granular collateral. A consumer loan pool might contain tens of thousands of obligors. A receivables book might span hundreds of customers. No single asset matters much, and statistical assumptions about default and recovery hold because the law of large numbers is doing real work.

Self-liquidating cash flows. The assets amortise or convert to cash on their own schedule. Receivables get paid. Loans amortise. The lender is repaid by the natural life of the collateral, not by a refinancing or a sale.

A monitored borrowing base. Advance rates are set against eligible collateral and recalculated frequently, often monthly and sometimes daily. As the pool shrinks or deteriorates, the facility shrinks with it.

Structural protections. Eligibility criteria, concentration limits, and performance triggers let the lender cut exposure before losses crystallise.

The result is a lending model where high advance rates are rational. Lending 85 per cent against a pool of investment-grade receivables is not aggressive. The granularity, the monitoring, and the contractual repayment make it safe.

Where NAV lending fits

NAV lending is non-recourse or limited-recourse credit secured against a defined pool of assets, with an advance rate set against the value of that pool. On those terms, it is squarely a form of asset-backed lending. The facility is ring-fenced from the borrower's other obligations, the lender looks to the collateral rather than a corporate covenant package, and sizing is driven by loan-to-value.

That is where the resemblance ends. The collateral in a NAV facility is private equity: fund interests, portfolio company holdings, or a family office's direct positions. Equity collateral behaves nothing like a receivables pool, and the differences cut across every dimension that makes classic asset-backed lending work.

The collateral is appraised, not contractual. A receivable has a face value and a due date. A portfolio company has a quarterly mark produced by the manager who owns it, usually arriving with a lag. There is no contractual cash flow to lend against, only an estimate of value.

Concentration is the norm. A NAV facility might be backed by eight or ten portfolio companies, sometimes fewer. The diversification mathematics that underpin securitisation simply do not apply. One bad outcome moves the whole collateral pool.

Repayment depends on exits. In classic asset-backed lending, the assets pay the lender down as they convert to cash. In NAV lending, repayment comes from realisations, and realisations depend on M&A and IPO windows that open and close with the cycle. The lender is taking duration and exit-market risk that asset-backed structures are specifically designed to avoid.

Enforcement is messier. An ABL lender can collect a receivables book. A NAV lender holds security over distribution accounts and equity in holding vehicles. You cannot liquidate a fund interest the way you collect an invoice.

The advance rate tells the story

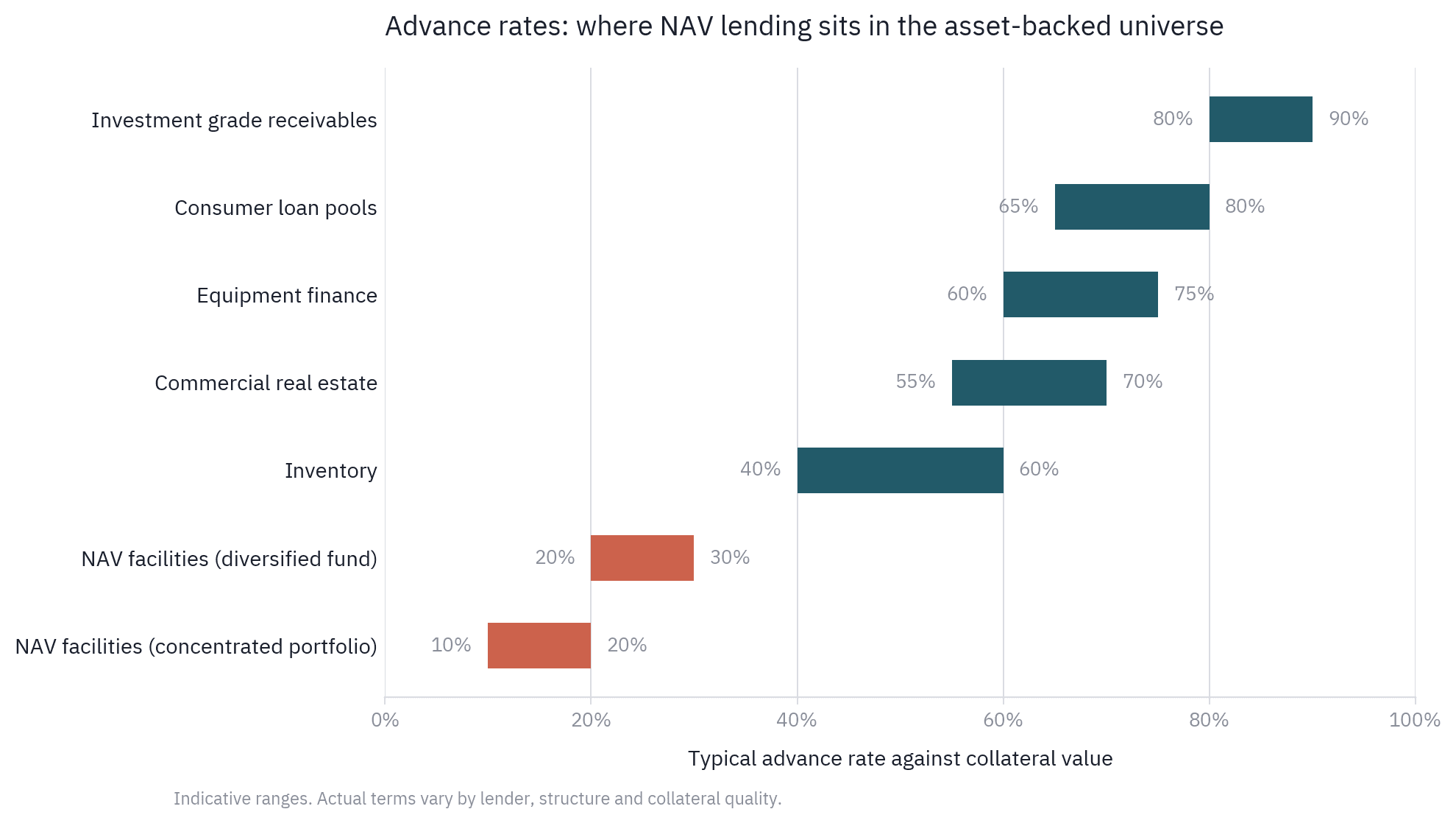

The clearest way to see the difference is to look at how much lenders will actually advance against each type of collateral.

Indicative advance rate ranges across the asset-backed lending universe. NAV facilities sit well below traditional ABL collateral types.

Investment-grade receivables support advance rates of 80 to 90 percent. Equipment and consumer pools sit between 60 and 80 percent. NAV facilities against diversified fund portfolios typically run at 20 to 30 percent, and against concentrated portfolios at 10 to 20 percent. These are not different points on the same risk curve. They are different lending models. In classic asset-backed finance, granularity and monitoring protect the lender, so the advance rate can be high. In NAV lending, the loan-to-value cushion is doing the work that granularity does elsewhere.

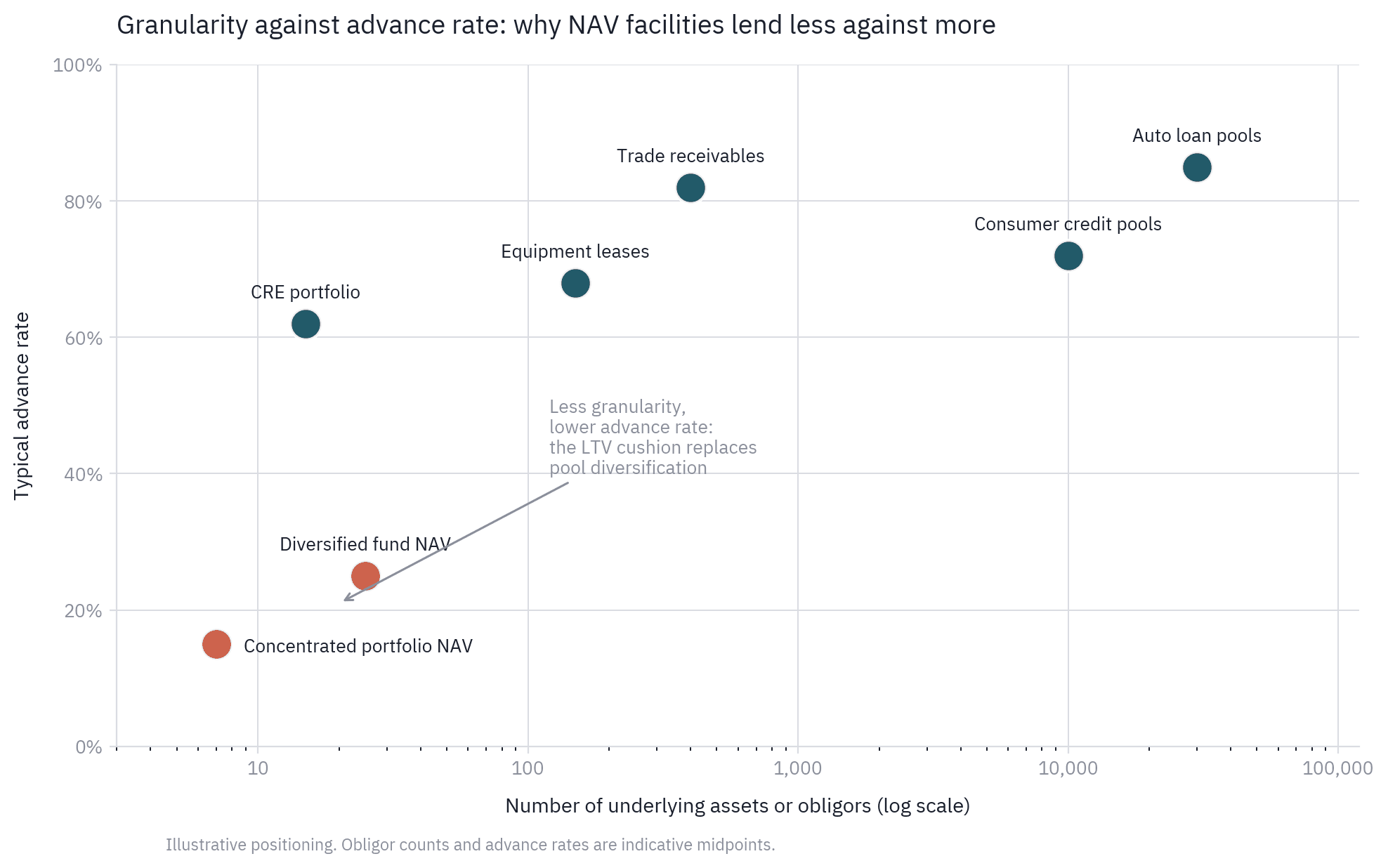

As collateral granularity falls, advance rates fall with it. In NAV lending, the LTV cushion replaces pool diversification as the lender's protection.

Plotting collateral granularity against advance rates makes the trade explicit. As the number of underlying assets falls from tens of thousands to single digits, the advance rate falls with it. A NAV lender advancing 15 percent against seven portfolio companies is not being conservative for the sake of it. The lender has no pool statistics to rely on, no monthly borrowing base to enforce, and no amortisation schedule baked into the collateral. The cushion is the protection.

Why the distinction matters

For borrowers, understanding the difference explains why NAV facility terms look the way they do. The diligence is bottom-up analysis of individual portfolio companies rather than pool stratification. The covenants are LTV and NAV maintenance tests rather than borrowing-base eligibility. The pricing reflects equity valuation risk and exit timing, not pool performance.

For allocators, the distinction matters more. Bucketing NAV lending inside an ABF allocation imports assumptions that do not hold. The risk in a NAV book is not obligor default in a granular pool. It is correlated equity marks, concentrated positions, and realisation timing. A NAV portfolio and a specialty finance portfolio can carry the same label and behave entirely differently in a downturn.

It also matters for pricing. Spreads in NAV lending are often quoted off the same mental grid as diversified asset-backed risk, which means concentrated NAV exposure is frequently priced as if pool diversification were present when it is not. The risk in NAV lending is not the product. It is the price, and the price only makes sense when the collateral is analysed for what it actually is: concentrated, appraised, exit-dependent private equity.