Why a bank will not lend against your private equity book

CRR3 risk weights, collateral eligibility rules, and balance sheet constraints explain why your private bank cannot offer what you need.

You hold a diversified private equity portfolio. Fund LP stakes across vintages and managers, a few co-investments and directs, perhaps EUR 50m to EUR 100m of net asset value. You ask your private bank for a facility at a conservative loan-to-value. The answer is often no. Where it is yes, the terms reflect the capital cost: broader recourse to your personal balance sheet, conservative sizing, or pricing that makes the facility uneconomic. This is not a judgment on the quality of your assets. It is a function of how banks are required to hold capital against them.

The collateral does not count

A bank does not look at your portfolio the way you do. It looks at what the rules permit it to recognise. Under the Capital Requirements Regulation, a lender seeking to reduce its capital charge by pledging collateral may do so only for assets on a defined list. The financial collateral comprehensive method, set out in Articles 197, 207 and 223 to 228, recognises cash, gold, debt securities with eligible ratings, equities in a main index, other equities traded on a recognised exchange, and units in funds that are priced daily and themselves hold only eligible instruments.

Private equity LP interests appear on none of these lists. They do not trade on an exchange. Secondary market indicative pricing exists, but does not satisfy the daily public price quote requirement. A closed-end PE fund is not an eligible collective investment for collateral purposes. Your co-investments and directs are unlisted shares with transfer restrictions and no observable price.

The consequence is direct. For capital purposes, the pledge over your portfolio counts for nothing. The bank must risk-weight the loan as if it were unsecured, based on the borrower's credit standing. Where that borrower is a holding company or an SPV with no operating cashflow, the covenant is thin, and the credit committee prices it accordingly.

Wrong-way risk closes the second door

There is a further problem that survives even if you try to argue the eligibility point. Article 207(2) requires that the credit quality of the obligor and the value of the collateral not have a material positive correlation. In a NAV facility the borrower's capacity to repay is the portfolio. If the portfolio falls, the borrower weakens at the same moment the security weakens. The framework treats that correlation as a reason to discount the protection, not credit it. It is the opposite of the diversified, independent collateral the rules are built around.

If the bank structures for the underlying economics, the charge is punitive

These are not academic distinctions. Some banks have attempted to structure PE-backed facilities as funded sub-participations or synthetic trades that give them the economic return on the underlying assets. When they do, the capital framework treats them as holding the asset itself, and the equity rules under CRR3 are severe.

The standardised approach assigns a 250 per cent risk weight to equity exposures generally, rising to 400 per cent for speculative unlisted holdings, with the higher figures phasing in across the EU between 2026 and 2030. Where the bank holds fund units and cannot look through to the underlying positions, and most offshore PE structures will not qualify for the look-through approach under Article 132, it applies the fall-back risk weight of 1250 per cent. At that level, the bank holds capital equal to the entire amount it has lent.

Banks cannot model their way out of this. CRR3 removes the internal ratings-based approach for equity exposures, so the standardised numbers apply directly. Even where models survive for the corporate loan treatment, the output floor rising to 72.5 percent by 2030 prevents them from softening the overall capital burden.

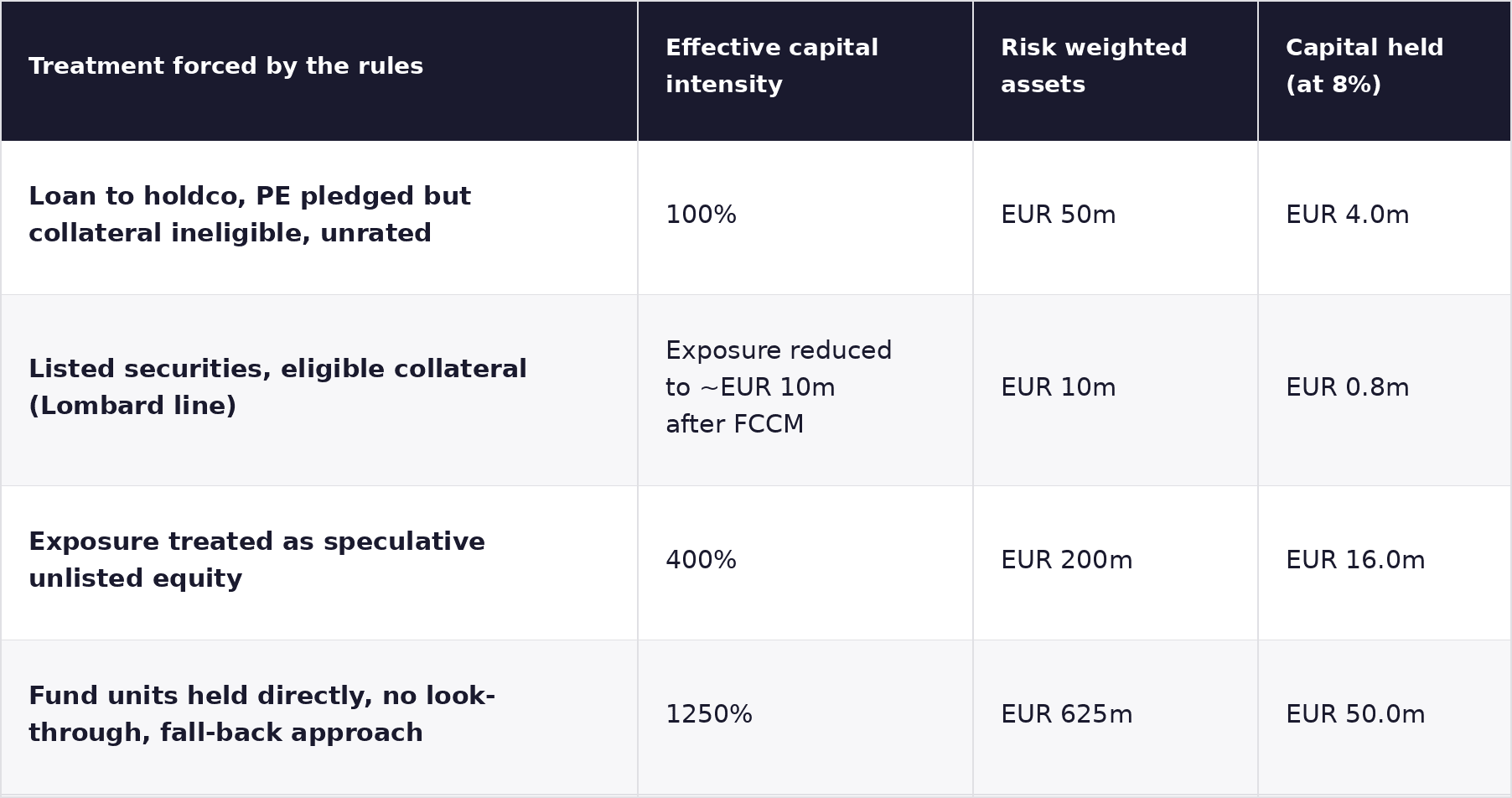

What this does to a EUR 50m facility

The table below shows how the same EUR 50m sits on a bank balance sheet depending on how the rules force it to be treated. Capital held is shown at the 8 percent own funds minimum. In practice, with the capital conservation buffer and an internal management add-on, most banks run an effective hurdle nearer 12 to 14 percent, so the real numbers are higher again.

Three constraints sit on top

Even when the bank accepts the base-case capital charge for an unrated corporate loan, three further constraints limit its appetite.

The large exposures regime under Article 395 caps what a bank can hold against a single counterparty or connected group at 25 percent of its Tier 1 capital, which bites on concentrated facilities. The leverage ratio counts the gross exposure regardless of risk weight, so the loan consumes capacity even where the credit is comfortable. The net stable funding ratio requires the bank to hold stable funding equal to the full amount of any loan with a residual maturity of more than 1 year. A PE facility with a seven to ten-year horizon consumes maximum NSFR capacity.

There is also the question of your unfunded commitments. An LP portfolio carries future capital calls that rank ahead of any lender and can force selling at the wrong moment. A deposit-funded balance sheet is poorly suited to carrying that contingency for years.

Why Nodem Capital is Different

Put together, this is where the private bank route ends. The assets a bank can lend against efficiently are liquid, priced daily, rated, or exchange traded, and uncorrelated with the borrower. Your PE book is none of these, so you are offered a Lombard line against your listed securities, and the portfolio that matters is left out of the calculation.

A fund lender like Nodem starts from a different place. Nodem lends from committed fund capital, not a deposit-funded bank balance sheet. We operate under fund regulation with our own risk management framework, but the bank-specific capital rules that make this lending uneconomic for a deposit taker do not apply to our structure. Our capital is locked for the life of the strategy, so we can bear illiquidity rather than incur charges for it.

Free from regulatory capital equations, we underwrite based on the portfolio's actual economics. We can structure around capital calls and accept PIK where appropriate, setting loan-to-value against the assets rather than an eligibility list.

The bank's no is a balance sheet artefact. It is not a verdict on your portfolio. That distinction is the reason this market exists.